Getting turned down for a business loan because your credit file is empty is one of the most frustrating roadblocks an entrepreneur can face. You’ve put real work into your company, but lenders see a blank page where your credit history should be. According to the Small Business Administration, sole proprietors face serious challenges building separate business credit because there’s no legal separation between personal and business finances, forcing lenders to rely on personal scores instead. This article walks you through every practical step, from choosing the right legal structure to opening your first tradelines, so you can start building a business credit profile that actually gets you funded.

Table of Contents

- Why legal structure matters: LLCs, corporations, and sole proprietors

- Step 1: Prepare your business for credit building

- Step 2: Open initial tradelines and choose reporting vendors

- Step 3: Understand business credit bureaus and monitoring

- Step 4: Maintain and grow your business credit profile

- What most guides miss about building business credit

- Strengthen your credit journey with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal structure is crucial | Forming an LLC or corporation separates personal and business credit, making true business credit building possible. |

| Vendor selection matters | Only open accounts with vendors who report to business credit bureaus if you want your activity to count. |

| Monitor all major bureaus | D&B, Experian, and Equifax each have unique scoring criteria—check your profiles with all three. |

| Pay early, not just on time | Early payments to vendors and creditors build strong scores and boost approval odds. |

| Credit building takes time | A solid business credit profile usually takes several months of consistent, responsible activity. |

Why legal structure matters: LLCs, corporations, and sole proprietors

Before diving into the steps, let’s clarify why your business’s legal structure is the foundation everything else is built on.

If you’re operating as a sole proprietor, lenders treat your business as an extension of you personally. That means your business has no separate credit identity. When you apply for financing, lenders pull your personal credit score, and your personal financial mistakes can follow your business into every deal. It’s a risky position for scaling, and it gets harder to manage the bigger your business grows.

Forming an LLC or corporation changes the equation entirely. Your business becomes a legally separate entity with its own tax ID, its own bank accounts, and its own credit file. The SBA strongly recommends converting a sole proprietorship to an LLC before pursuing serious business credit, specifically because that legal separation is what makes true building credit history possible in the first place.

Here’s a quick look at how entity types compare when it comes to credit building:

| Entity type | Legal separation | Own credit profile | Personal liability |

|---|---|---|---|

| Sole proprietor | None | No | Full |

| LLC | Yes | Yes | Limited |

| S-Corp / C-Corp | Yes | Yes | Very limited |

Key advantages of forming an LLC before building business credit:

- Your business can open its own bank accounts and credit lines

- Lenders and vendors see your business as a standalone borrower

- Business mistakes don’t automatically damage your personal credit

- You qualify for business-specific credit products and vendor terms

- Your personal assets are protected from most business liabilities

Pro Tip: Don’t wait until you’re ready to apply for a large loan to form your LLC. The sooner your business has its own legal identity, the sooner your credit clock starts ticking. Most states process LLC filings within a few business days, and the cost is typically under $200.

Exploring creative building credit ideas becomes far more productive once your business is properly structured. If your current credit situation needs work alongside your business setup, understanding building credit repair strategies can help you address both tracks at once.

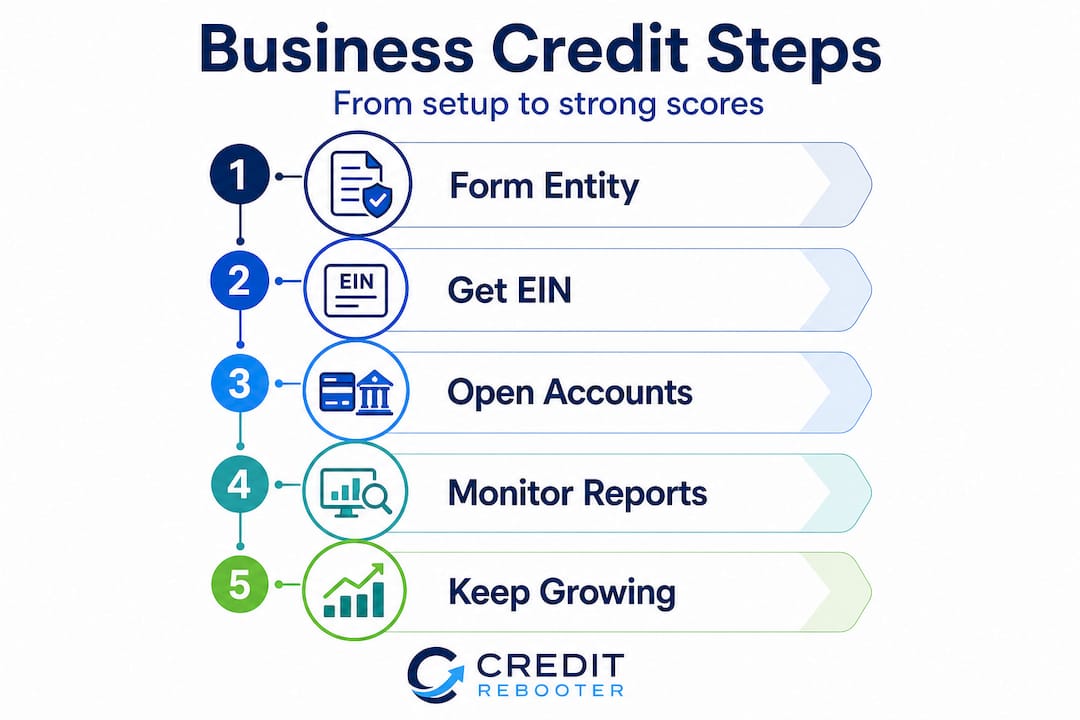

Step 1: Prepare your business for credit building

With your legal structure in place, it’s time to gather the right tools and documentation before opening any credit accounts.

Think of this stage as setting up your business’s identity on paper. Lenders and vendors need to verify that your business is real, consistent, and organized before they’ll extend credit to it. Missing even one piece of this foundation can delay your credit file from forming or cause reporting errors that hurt you later.

Here’s what you need in place before opening your first credit account:

- Get an Employer Identification Number (EIN). This is your business’s equivalent of a Social Security number. Apply free at IRS.gov and use it on every business document, account, and application.

- Open a dedicated business bank account. Use your EIN and legal business name. This account should be completely separate from your personal finances. Even small deposits and expenses should run through it.

- Set up a business phone number and address. These need to be consistent across all filings. A virtual office address works, but it must match what’s listed on licenses and credit applications.

- Register your business with Dun & Bradstreet. Getting a DUNS number is essential. Most major business credit bureaus and vendors require one before they’ll report your payment activity to your file.

- Verify consistency across all records. Your business name, address, phone, and EIN must match exactly on every document, every time. Inconsistencies cause reporting gaps and can delay your credit file.

The following table shows the key setup items, where to get them, and why each one matters:

| Setup item | Where to obtain | Why it matters |

|---|---|---|

| EIN | IRS.gov (free) | Separates business from personal identity |

| Business bank account | Any bank or credit union | Shows financial separation to lenders |

| DUNS number | Dun & Bradstreet (free) | Required for most vendor and bureau reporting |

| Business license | State or local government | Validates legitimacy |

| Business phone/address | Virtual office or physical location | Needed for consistent records |

As the SBA advises, your personal credit will still matter initially, especially for small loans. That’s why working on both simultaneously pays off. Our business credit checklist covers every document you’ll need in one place. If you’re just getting started, establishing credit from scratch requires patience but follows a predictable path when you stay organized. Once you’re set up, building and using business credit effectively becomes much more straightforward.

Step 2: Open initial tradelines and choose reporting vendors

Once your business records and DUNS are set up, you’re ready to start the process of actually building credit with your first tradelines.

A “tradeline” is simply a credit account that gets reported to a bureau. Every time a vendor extends you net 30 or net 60 payment terms and reports your payment behavior, that’s a tradeline. The more positive tradelines you have, the stronger your business credit file becomes.

The catch that catches most entrepreneurs off guard? Not all vendors report your payment activity. You could be buying supplies on credit from a vendor for two years and have zero activity show up on your business credit file. Before opening any account for credit-building purposes, ask the vendor directly whether they report to D&B, Experian, or Equifax Business.

Best practices for opening starter tradelines:

- Target 2 to 5 vendors who are confirmed to report to at least one major bureau

- Use vendors in categories your business actually needs, such as office supplies, shipping, or industrial equipment

- Pay invoices 10 to 15 days early whenever possible, not just on time

- Keep balances and usage consistent so your file shows steady activity

- Avoid opening too many accounts at once, which can look unstable to lenders

Why early payment matters: Your PAYDEX score from Dun & Bradstreet is a 0 to 100 score where 80 represents on-time payment and 100 represents early payment. Paying just a few days early can be the difference between a score that impresses lenders and one that merely satisfies them.

According to the BizBake Business Credit Guide, starter vendors in office supplies such as Uline, Quill, and Grainger are popular choices specifically because they report to the major bureaus and extend terms to newer businesses. The guide also recommends paying 10 to 15 days early to optimize your PAYDEX score, and warns that reporting can lag by several weeks to months, so patience is essential.

Pro Tip: When you call a vendor to ask if they report payment activity, also ask which bureau they report to. Some vendors only report to D&B, others to Experian or Equifax. Diversifying across bureaus gives you a stronger overall profile.

Working on smart credit building strategies from the beginning means you won’t waste months on accounts that never show up on your report.

Step 3: Understand business credit bureaus and monitoring

After opening accounts, it’s essential to understand how your actions get translated into business credit reports and scores.

Business credit doesn’t work like a single FICO score. There are multiple bureaus, each with their own scoring models, and lenders may check any one or all of them. Knowing how each bureau thinks helps you make smarter decisions about which behaviors to prioritize.

Here’s how the major business credit bureaus stack up:

| Bureau | Score name | Range | What they focus on |

|---|---|---|---|

| Dun & Bradstreet | PAYDEX | 1 to 100 | Payment timeliness |

| Experian Business | Intelliscore Plus | 1 to 100 | Broader risk prediction |

| Equifax Business | Business Credit Risk Score | 101 to 992 | Delinquency risk |

| FICO | SBSS (Small Business) | 0 to 300 | Blends personal and business data |

As Capital One’s business credit guide explains, D&B focuses on payment history through PAYDEX, Experian uses a broader risk model called Intelliscore, Equifax emphasizes delinquency risk, and the FICO SBSS score blends both personal and business credit data, which is what many SBA lenders use to evaluate applications.

“Your business credit score is not just a number. It’s a snapshot of your company’s financial habits, reliability, and risk level. Lenders use it to decide not just whether to approve you, but how much to lend and at what rate.”

Understanding your scores at all three bureaus means checking them regularly. Unlike personal credit, you typically pay to access your business credit reports. Budget for monthly or quarterly monitoring so you catch errors, identity fraud, or stale data before it affects a loan application. Use understanding credit bureaus resources to get a clear picture of how each bureau evaluates your file and what steps move your score in the right direction.

Step 4: Maintain and grow your business credit profile

With your credit file established, maintaining and steadily building on it ensures lenders will view your business more favorably over time.

Many entrepreneurs do the hard work of setting up their credit foundation and then let momentum carry them, without realizing that business credit requires active management. Dormant files, inconsistent payments, or a thin number of tradelines can stall progress or even hurt your standing with lenders.

Here’s how to stay on track once your profile is active:

- Pay every invoice early, not just on time. This is especially critical for PAYDEX. Even one late payment can drop your score significantly and stay on your record.

- Add new tradelines gradually. Once you have 3 to 6 months of history, start adding a business credit card. Use it regularly and pay the balance in full each month.

- Review your business credit reports monthly. Errors happen more than you’d think. A vendor might report incorrect payment dates or amounts, and fixing those errors takes time.

- Address disputes quickly. If you spot inaccuracies, file disputes with the relevant bureau immediately. Unresolved errors can linger and create problems when you apply for financing.

- Keep your business information consistent. Any change to your address, phone number, or legal name needs to be updated with every bureau and vendor at the same time.

According to the BizBake Business Credit Guide, new businesses should start with 2 to 5 reporting tradelines plus one business credit card, and scores typically emerge within 3 to 6 months of consistent early payments. The guide also makes a critical point: having no credit file at all is actually riskier in the eyes of lenders than having a low score, because a low score at least tells them something.

Pro Tip: Set a recurring monthly calendar reminder to log in and check your business credit reports. Treat it like reviewing your bank statement. Catching a reporting error three months later instead of immediately can push back a loan application by months.

If things have gone sideways at any point, repairing business credit is absolutely possible with the right approach. Start by understanding credit files and identifying exactly where the damage is before taking action.

What most guides miss about building business credit

Here’s the part most credit guides gloss over, and it’s where most entrepreneurs quietly make their biggest mistakes.

The standard advice, which we’ve covered above, is solid. But the real challenge isn’t knowing the steps. It’s managing your expectations and avoiding the psychological traps that come with waiting for results.

Most new business owners spend time worrying about having a low score. What they should be worrying about is having no score. A thin credit file with very few tradelines and minimal history is actually a bigger red flag to lenders than a modest score with real activity behind it. Lenders can’t evaluate risk when there’s nothing to evaluate. They pass, every time.

The second trap is chasing shortcuts. You’ll find vendors selling “shelf corporations” or “tradeline rentals” promising to fast-track your business credit. Some are outright scams. Others produce short-term numbers that collapse under any real lender scrutiny. Sustainable credit health comes from consistent behavior, not clever workarounds.

The third mistake is overextending too fast. Opening 10 accounts in your first month looks desperate, not established. Lenders look at the age of your accounts and the breadth of your relationships. Growing steadily over 12 to 18 months tells a better story than cramming activity into a few weeks.

The truth is that building strong business credit is closer to building a reputation than building a resume. Every payment you make on time, every account you manage responsibly, adds to a track record that lenders eventually trust. Our comprehensive credit checklist gives you a structured way to track that progress without skipping steps or chasing fast results.

Patience isn’t a passive strategy. It’s the most effective one available.

Strengthen your credit journey with expert support

You now have a clear roadmap for building business credit from the ground up. But knowing the steps and executing them perfectly, while also running a business, are two very different challenges.

Professional guidance can save you months of trial and error, help you avoid the reporting mistakes that stall credit files, and point you toward the smartest next moves for your specific situation. Whether you’re starting fresh, recovering from past credit problems, or trying to accelerate your path to better financing, Credit Rebooter has the tools and expertise to support you. Explore our business credit strategies and learn how to fast-track building your business credit history with a system that’s designed for real results, not guesswork.

Frequently asked questions

How long does it take to build business credit?

With 2 to 5 active tradelines and consistent on-time payments, scores can emerge in as little as 3 to 6 months. Building a strong, lender-ready profile typically takes 12 to 18 months of steady activity.

Do I need a DUNS number to start building business credit?

Yes. The SBA recommends getting a DUNS number first, as most business credit bureaus and vendors require one before they’ll report your payment activity to your file.

Will my personal credit still be used for business loans at first?

Personal credit still matters initially for small loans, especially when your business credit file is new or thin. That’s why managing both personal and business credit simultaneously is a smart early strategy.

Which vendors are best for starting business credit?

Office supply vendors such as Uline, Quill, and Grainger are popular starter options because they extend terms to newer businesses and report to D&B, Experian, or Equifax Business. Always confirm reporting before opening an account.

What hurts business credit the most?

Late payments and a lack of credit history are the biggest red flags. As the BizBake guide notes, having no file at all is riskier than having a low score, because lenders have nothing to base a decision on.