You make your final payment on a credit card, feel great about it, then open your credit monitoring app a week later to find your score dropped by 15 points. That scenario is more common than you think, and it catches both individuals and small business owners completely off guard. Credit scores don’t operate on logic you can see at a glance. They respond to mechanics, timing, and formulas that often produce results that feel backward. This guide cuts through the confusion and gives you a practical framework for understanding why your score moves and what you can actually do about it.

Table of Contents

- What makes your credit score change?

- Why good actions sometimes lower your score

- Business credit scores: Why changes happen and how to monitor them

- How to respond to credit score changes: Practical steps

- What most credit guides miss: Why chasing instant improvement can backfire

- Take control of your credit score with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Not all changes are bad | Credit score drops can happen after positive moves like paying off debt due to reporting mechanics. |

| Timing matters | Pay attention to your creditors’ reporting dates for effective score management. |

| Business scores are complex | Business owners must track multiple bureaus and focus on timely payments for stable credit. |

| Respond strategically | Have a checklist to address changes and avoid quick, emotional decisions. |

| Long-term habits win | Consistent, reliable financial practices drive lasting credit improvement—not chasing scores. |

What makes your credit score change?

Credit scores are not a single number assigned by one authority. For personal credit, the most widely used models are FICO and VantageScore, and both pull data from three major bureaus: Equifax, Experian, and TransUnion. Each bureau may have slightly different information at any given moment, which is why your score can vary depending on which one a lender checks.

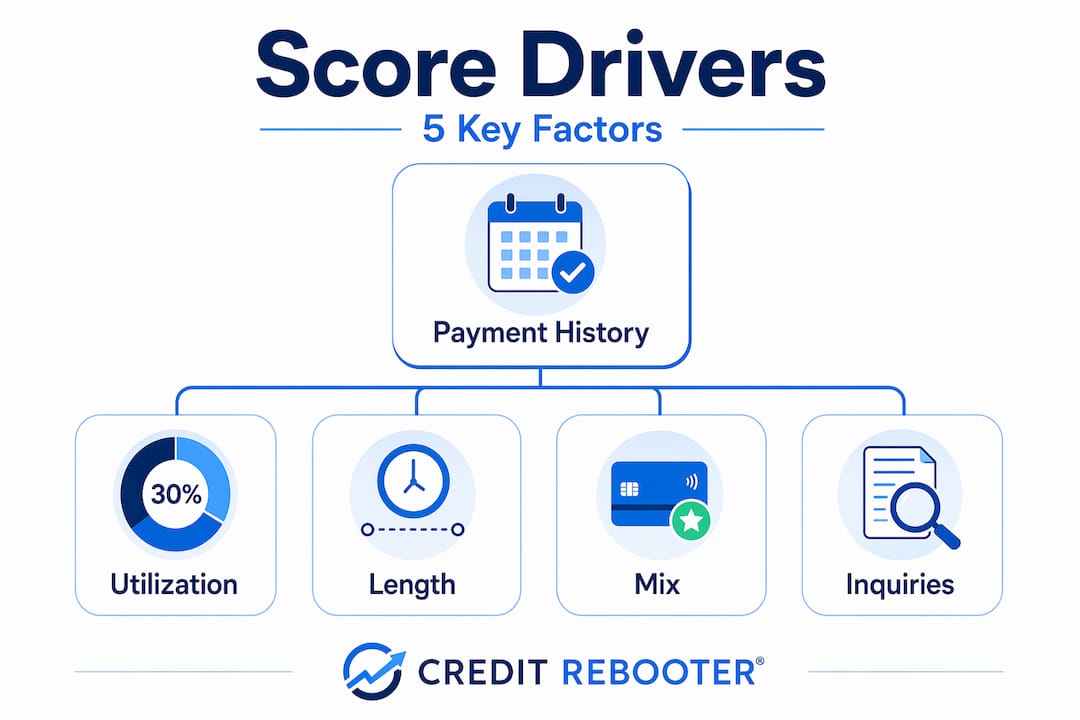

The five core factors that move your personal credit score are payment history, credit utilization, length of credit history, credit mix, and new credit inquiries. Payment history carries the most weight, typically around 35% of your FICO score. Credit utilization, which is the percentage of your available revolving credit you’re currently using, comes in second at roughly 30%. These two factors alone account for nearly two thirds of your score.

Here’s where things get counterintuitive. As the reasons credit scores fluctuate often show, even positive events can drag your score down temporarily. Paying off a credit card and then closing it removes that card’s credit limit from your total available credit. Your utilization ratio rises even though your debt went down. As WTOP explains, your score can drop after you pay off accounts because of reporting mechanics and credit mix shifts. The math matters more than the intention.

For business credit, the mechanics are different but equally important. Business scores use different models entirely, including Dun & Bradstreet’s PAYDEX, Experian’s Intelliscore Plus, and the FICO Small Business Scoring Service (SBSS). Each model weighs factors differently and business scores change with newly reported information and bureau-specific factors.

| Action | Factor Affected | Likely Score Impact |

|---|---|---|

| Paying off and closing a card | Utilization, credit mix | Short-term drop |

| Making on-time payments | Payment history | Gradual improvement |

| Opening a new account | Hard inquiry, average age | Temporary dip |

| Reducing revolving balances | Utilization | Improvement |

| Public record filed (lien, judgment) | Payment history/public records | Significant drop |

| Adding a new vendor tradeline (business) | Payment data | Can improve over time |

Key factors to track for personal scores:

- Credit utilization ratio (keep it under 30%, ideally under 10%)

- Payment history (even one missed payment can cost 50 to 100 points)

- Average age of accounts (older accounts help your score)

- Hard inquiries (too many in a short window signal risk)

- Credit mix (a combination of revolving and installment accounts helps)

Why good actions sometimes lower your score

Understanding the mechanics is key, but let’s explore why even the “right” moves aren’t always instantly rewarded.

The most common source of frustration is the reporting cycle. Your credit card issuer doesn’t report your balance to the bureaus in real time. They typically report once a month, often on or around your statement closing date. So if you pay off your entire card balance today but your issuer doesn’t report for another three weeks, the bureaus still see the old, higher balance. Your score reflects the old data until the update comes through.

This timing gap is one of the most underappreciated mechanics in credit scoring. Paying off revolving debt can improve scores, but timing matters due to reporting cycles and utilization formula changes. If you’re applying for a mortgage or auto loan within the next 30 days, that delay could cost you real money in the form of a higher interest rate.

Closing accounts creates another trap. Many people assume that closing a card they no longer use is responsible financial behavior. It is, emotionally. But from a scoring standpoint, that closed card takes its credit limit off the table. If you had $10,000 in total credit limits and $2,000 in balances, your utilization was 20%. Close a card with a $4,000 limit and now your total available credit drops to $6,000. Your utilization jumps to 33%, and your score takes a hit through no fault other than the math.

“Your credit score doesn’t reward good intentions. It rewards specific behaviors at specific times. Understanding the difference between what you did and when the system registers it is the real skill.” — Credit Rebooter

Here’s a side-by-side comparison of common actions and their effects:

| Action | Immediate effect | Longer-term effect |

|---|---|---|

| Paying off a card (keeping it open) | Possible short-term drop from reporting lag | Score improves once updated |

| Closing a paid-off card | Utilization rises, score drops | Continued impact on credit history length |

| Opening a new credit card | Hard inquiry lowers score slightly | Raises available credit, lowers utilization over time |

| Paying off an installment loan | Removes from credit mix, slight dip | Reflects positively in payment history |

The ways to improve your credit score that actually work long term aren’t always the ones that feel most satisfying in the moment.

Pro Tip: Call your credit card issuer and ask exactly which date they report your balance to the bureaus. Pay your balance down before that date each month, and your reported utilization will be lower even if you use the card heavily the rest of the month.

Business credit scores: Why changes happen and how to monitor them

While personal scores seem tricky, business credit introduces a new layer of complexity that’s vital for entrepreneurs.

Unlike personal credit, business credit is not protected by the same federal regulations. There’s no legal requirement for vendors or suppliers to report your payments at all. Many don’t. This means your business credit profile can be surprisingly thin even if you’ve been operating for years and paying everyone on time.

When a vendor does report, it can shift your score significantly. The D&B, Experian, and Equifax business bureaus each weight factors differently and update at different times. D&B’s PAYDEX score, for example, is based entirely on payment performance relative to terms. Pay early and you can score above 80 on a scale of 100. Experian’s Intelliscore Plus considers more factors including public records and industry risk. That means your scores across bureaus can look dramatically different even with identical payment behavior.

Public records hit business credit especially hard. A tax lien, a judgment, or even a UCC filing can dramatically lower your score overnight. These are searchable in public databases and are automatically pulled into bureau reports. Small business owners are often blindsided by this because they don’t monitor business credit the way they watch personal scores.

How to effectively monitor your business credit:

- Pull your D&B, Experian Business, and Equifax Business reports at least quarterly

- Ask vendors directly whether they report to any bureau, and which one

- Set calendar reminders for payment due dates that include a three-day buffer for processing

- Watch for UCC filings if you have equipment financing or SBA loans

- Register your business on D&B’s portal to claim your profile and correct errors early

A powerful statistic worth knowing: timely payment is the number one factor for business credit across all bureaus. It seems obvious, but many small business owners prioritize cash flow over credit payments during tight months, not realizing the downstream cost in financing rates and vendor terms.

For a complete roadmap, the business credit best practices that experienced entrepreneurs use can shorten the learning curve considerably. You should also understand how your credit report and score interact before applying for any business financing.

Pro Tip: If you want vendors to report your payments to business bureaus, ask them directly. Some vendors will add you to their reporting roster upon request, especially if you have a strong payment history with them.

How to respond to credit score changes: Practical steps

With the reasons for score changes clear, let’s make sure you know exactly what to do next, step by step.

For individuals: A practical response checklist

- Pull your credit reports from all three bureaus. You’re entitled to free weekly reports at AnnualCreditReport.com. Look for accounts you don’t recognize, incorrect balances, and wrong personal information.

- Identify your reporting dates. Log into each card account and find the statement closing date. This is usually when balances are reported.

- Calculate your utilization ratio. Add up all your credit limits, then add up all your balances. Divide the total balance by the total limit. If it’s over 30%, focus on paying it down before your next reporting date.

- Avoid closing old accounts prematurely. If a card has no annual fee, leave it open. A zero-balance open account helps both your utilization ratio and your average account age.

- Dispute errors immediately. The improving your credit score process stalls when errors on your report pull the score down unfairly. File disputes online directly with each bureau.

- Space out credit applications. Each hard inquiry can lower your score by a few points. If you’re shopping for a mortgage or car loan, do it within a 14-day window so multiple inquiries count as one.

For business owners, the strategy is similar in spirit but different in execution. The SCORE resource on business credit recommends setting up systems for monitoring, on-time payments, and understanding what triggers bureau reports. And as TD Bank’s guidance on utilization timing confirms, for quick score improvements, managing utilization and timing payoffs to match reporting cycles is the most efficient path.

Common mistakes to avoid:

- Obsessing over every small score movement (scores fluctuate naturally by 5 to 20 points month to month)

- Ignoring your reporting schedule and then wondering why your score hasn’t improved yet

- Closing accounts to “simplify” your finances without checking the utilization impact first

- Applying for multiple credit lines in a short window outside of rate-shopping scenarios

- Assuming business credit will build itself without intentional vendor and bureau management

For practical tools and useful tips to raise scores, building a monthly review habit is far more effective than reacting emotionally to every score notification.

What most credit guides miss: Why chasing instant improvement can backfire

Most articles on credit scores read like instruction manuals. They tell you the five factors, remind you to pay on time, and send you on your way. What they miss is the behavioral reality of how people actually interact with their scores.

Credit monitoring apps have made scores feel like a stock ticker. People check them daily. They make decisions based on single-point moves that are statistically meaningless. We’ve seen it countless times: someone opens two new cards to boost their available credit, triggers two hard inquiries, drops their average account age, and ends up with a lower score than when they started.

The real risk isn’t a temporary score drop from paying off a card. The real risk is developing a reactive relationship with your credit, where every dip triggers a defensive move that creates new problems. Opening and closing accounts frequently does lasting structural damage to your credit profile that takes years to heal.

True credit health is boring. It’s consistent, on-time payments month after month. It’s keeping utilization low without overthinking it. It’s leaving old accounts open and not applying for new credit unless there’s a strategic reason. It’s the kind of discipline that doesn’t show up in a flashy score jump but shows up when a lender sees five years of spotless history and offers you their best rate.

For lasting credit improvement, the mindset shift matters as much as the tactics. Stop asking “how do I raise my score this month?” and start asking “what does my credit profile look like to a lender two years from now?” That perspective change will do more for your financial life than any quick fix.

Take control of your credit score with expert support

Navigating credit score changes on your own can feel like reading a manual in the dark. You now understand why scores move, what triggers short-term drops, and how to respond strategically for both personal and business credit.

If you’re ready to move from understanding to action, Credit Rebooter offers structured support designed for exactly where you are right now. Whether you’re dealing with unexplained drops, working through bad credit repair solutions, or building a long-term strategy using proven credit score repair strategies, there’s a clear path forward. Our credit repair system gives you both the education and the tools to take meaningful action, not just read about it.

Frequently asked questions

Can my credit score drop after paying off debt?

Yes, paying off debt, especially by closing a credit account, can reduce your available credit and temporarily lower your score due to mechanics like reduced available credit and credit mix changes.

Why does my business credit score change so often?

Business scores shift frequently because bureau models differ in how they weight payment data, public records, and account updates, and each bureau reports on its own schedule.

How fast can I increase my credit score?

You can often see improvements in 30 to 60 days by reducing credit utilization, but reporting schedules impact timing since issuers only update balances to bureaus once a month.

What’s the most important factor for my business credit?

Timely payments to creditors and vendors are the top factor across D&B, Experian Business, and Equifax Business scoring models.

Should I worry about every small score drop?

Minor score drops are completely normal and often self-correct within one to two billing cycles. Focus on consistent, positive habits rather than reacting to every small change your monitoring app shows you.