Your credit score follows you everywhere. Apply for a mortgage, rent an apartment, finance a car, or open a business line of credit, and that three-digit number either opens the door or slams it shut. The frustrating part? Ask ten different people what a “good” credit score is, and you’ll get ten different answers. Some say 700, others say 720, and a few will confidently tell you 750 is the bare minimum. This guide cuts through that noise by explaining the actual score ranges, the models behind them, and what “good” truly means when real money is on the line.

Table of Contents

- Credit score basics: What do the numbers really mean?

- FICO vs. VantageScore: How your score is really calculated

- What is considered a “good” credit score?

- How good credit scores open financial doors

- The truth most articles miss about credit scores

- Take your next steps to better credit

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Good score defined | A score of 670+ for FICO and 660+ for VantageScore is generally considered good. |

| Model differences matter | Your score can vary by 30-50 points depending on whether FICO or VantageScore is used. |

| Benefits of good credit | Good scores unlock better loan rates, housing, insurance, and business funding opportunities. |

| Personal and business credit | Small business owners often need strong personal and separate business credit for financing. |

| Focus on habits | Consistent positive credit behaviors are more valuable than reaching a single score threshold. |

Credit score basics: What do the numbers really mean?

A credit score is a numerical summary of your creditworthiness, calculated from the information on your credit report. Think of it as a financial report card that lenders, landlords, and insurers use to predict how likely you are to repay what you borrow. Scores generally run on a scale from 300 to 850, where higher always means better.

There are some facts about credit scores that surprise most people: your score is not a single fixed number. It changes depending on which scoring model is used and which credit bureau supplied the underlying data. That’s why you might see a 690 on one site and a 715 on another for the same day.

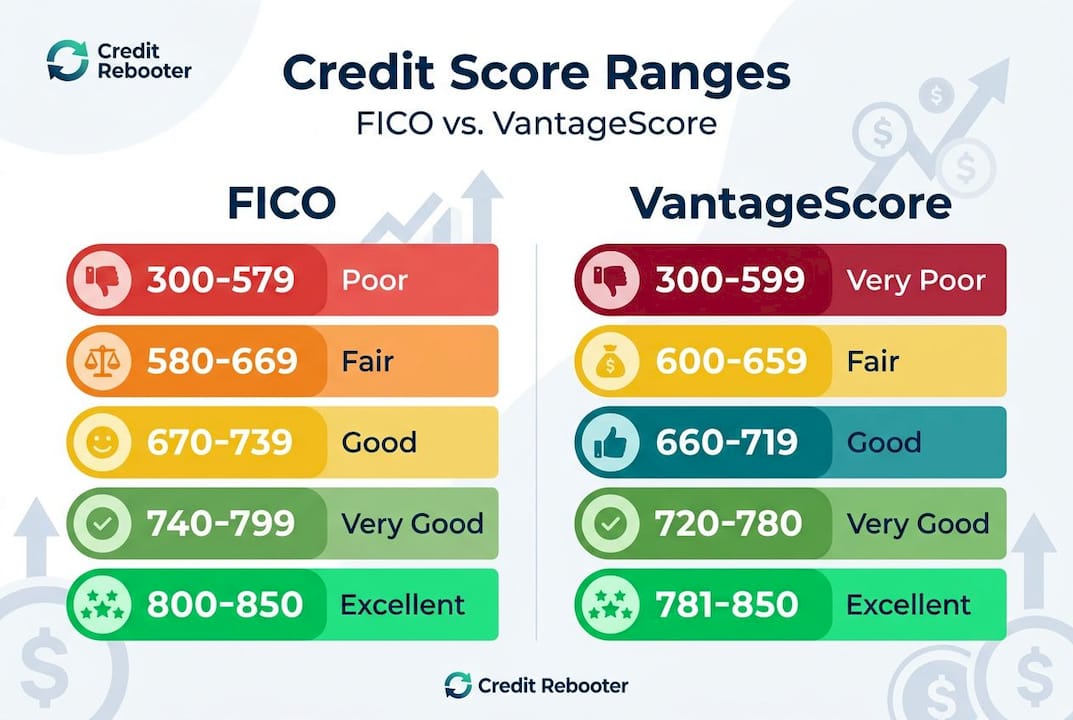

The two dominant models are FICO and VantageScore. FICO dominates roughly 90% of lending decisions, while VantageScore has grown in popularity, especially for consumers with limited credit histories. Both use the 300 to 850 scale, but they calculate your score differently.

Here is how both models classify score ranges, along with general implications:

| Score range | FICO label | VantageScore label | General standing |

|---|---|---|---|

| 300 to 579 | Poor | Very poor | High risk, frequent denials |

| 580 to 669 | Fair | Poor | Some approvals, high rates |

| 670 to 739 | Good | Fair | Most mainstream approvals |

| 740 to 799 | Very good | Good | Competitive rates widely available |

| 800 to 850 | Exceptional | Excellent | Best rates, easiest approvals |

Notice that the labels don’t perfectly match between models. That creates real confusion. A 680 is “good” under FICO but only “fair” under VantageScore. Knowing which model a lender uses before you apply is essential, because the same score can carry a very different label depending on where it is being read. You can review the full breakdown of credit score ratings to see how each tier stacks up across use cases.

Key factors that influence your score across both models include:

- Payment history: Whether you pay on time, every time

- Credit utilization: How much of your available credit you are actively using

- Length of credit history: How long your accounts have been open

- Credit mix: Having a variety of account types, such as cards, loans, and mortgages

- New credit inquiries: How many recent applications you have submitted

FICO vs. VantageScore: How your score is really calculated

Knowing the ranges is helpful, but understanding the models behind the numbers helps you make sense of your real score.

Both models look at your credit report, but they process it differently. These differences can produce a 30 to 50 point gap between your FICO score and your VantageScore on the same day, even with identical underlying data. That’s a significant difference when you’re sitting across from a loan officer.

Here is a side-by-side comparison of key calculation differences:

| Factor | FICO | VantageScore |

|---|---|---|

| Minimum history required | 6 months | 1 month |

| Credit utilization weight | ~30% | ~20% |

| Paid collections | Counted in older versions | Ignored in Version 3.0 and above |

| Trended data | Used in FICO 10T | Used in Version 4.0 |

| Rate shopping window | Up to 45 days (same loan type) | 14 days |

Let’s walk through what these differences actually mean for you:

-

Thin file treatment. If you are new to credit, VantageScore scores thin files with as little as one month of history, while FICO requires at least six months. This means recent graduates or new immigrants may have a VantageScore but no FICO score at all initially.

-

Paid collections. Newer scoring models have changed how they treat collections accounts that you have already paid. Newer models ignore paid collections, specifically VantageScore 3.0 and higher, along with FICO 9 and above. But many lenders still use older FICO versions, so a paid collection could still hurt your score depending on which version they pull.

-

Trended data. Both FICO 10T and VantageScore 4.0 look at your credit behavior over time, not just a snapshot. If you have been steadily paying down a balance, that positive direction gets rewarded. Someone with the same current balance but an upward trend looks riskier under these models.

-

Rate shopping. Applying to multiple mortgage lenders in the same period is treated as one inquiry under FICO if done within 45 days. VantageScore only gives you 14 days. Knowing which window applies can save you score points when you’re shopping for the best rate.

The credit score scale and its relationship to these models is explained in more detail in our resources, but the core takeaway is this: the model matters as much as the number.

Pro Tip: Before applying for any major loan or credit line, ask the lender directly which scoring model and which version they use. This single question can help you prioritize the right improvements and avoid surprises at the closing table.

Understanding the credit score breakdown in detail gives you a major advantage because you stop treating your score as a mystery and start treating it as a system you can navigate.

What is considered a “good” credit score?

With both models in mind, let’s clarify exactly what number is generally accepted as “good” and why it matters.

Most lenders use FICO, and under that model, a score of 670 or above is where the “good” range officially begins. For VantageScore, that threshold sits at 660. These are not magic numbers, but they represent the general boundary where mainstream lenders start offering approvals without requiring additional conditions or unusually high interest rates.

Here is how score tiers typically affect your real-world opportunities:

| Score tier | Loan approval likelihood | Interest rate quality | Rental approval | Insurance impact |

|---|---|---|---|---|

| Below 580 | Very unlikely | Not applicable | Often denied | High premiums |

| 580 to 669 | Possible with conditions | High rates | May require extra deposit | Above average premiums |

| 670 to 739 | Likely | Moderate rates | Generally approved | Standard premiums |

| 740 to 799 | Very likely | Competitive rates | Easily approved | Discounts possible |

| 800 and above | Near certain | Best available rates | Strong preference | Best pricing |

Crossing from 669 into the 670 range is more than symbolic. FICO scores of 670 and above represent the threshold where most mainstream lenders shift from skepticism to confidence. You may still pay a higher rate than someone at 740, but your odds of approval improve dramatically.

Common factors that push scores higher include:

- Consistent on-time payment history over 24 months or more

- Credit utilization kept below 30%, ideally below 10%

- A mix of revolving credit and installment loans

- Old accounts kept open to lengthen average account age

- Fewer hard inquiries in the past 12 months

Common factors that pull scores lower include:

- One or more late or missed payments

- Maxed-out credit cards, even temporarily

- Recently opened multiple new accounts

- Collections accounts, even older ones in older scoring models

- A short credit history with only one account type

“The difference between a 660 and a 720 score is not just a number. On a 30-year mortgage, that gap can translate to tens of thousands of dollars in additional interest paid over the life of the loan.”

Landlords check scores too, often using a threshold between 620 and 680 depending on the rental market. In competitive cities, many landlords prefer 700 and above. Auto insurers in most states factor in your credit, and a score in the “good” range can meaningfully reduce your premium compared to someone in the “fair” range.

You can use a credit score chart to map your current number to specific outcomes and set a realistic target.

How good credit scores open financial doors

Now that you know what “good” means, here’s how reaching it directly benefits your financial opportunities.

For individuals, a good credit score means more than just loan approvals. It means better terms, lower monthly payments, and less financial stress over time. Consider a simple example: two people apply for a $25,000 auto loan. Person A has a 620 score and gets quoted 11% interest. Person B has a 720 score and qualifies for 6%. Over a five-year loan, Person B pays roughly $4,000 less in interest for the exact same car.

Benefits of reaching the “good” score range include:

- Access to mortgages with down payments as low as 3% to 5%

- Credit card approvals with cash back rewards and sign-up bonuses

- Apartment rentals without requiring a co-signer or double deposit

- Auto loan rates that save you thousands compared to subprime financing

- Lower monthly auto and renters insurance premiums

For small business owners, the equation is slightly more complex. Most lenders who evaluate small business loans look at both your personal credit score and your business credit profile. According to the SBA, building separate business credit using a DUNS number is important, but your personal score remains a critical factor in most lending decisions, especially for newer businesses.

A strong personal score acts as a character reference for your business in the eyes of lenders. If your business hasn’t built two to three years of credit history yet, your personal score often carries the entire application.

Pro Tip: Start building credit history for your business as early as possible. Open a business bank account, get a small business credit card, and register with business credit bureaus. But keep your personal score clean at the same time, because most small business lenders will check both.

Our business credit checklist walks through every step of establishing a separate business credit profile so you can qualify for better financing as your company grows.

The truth most articles miss about credit scores

You’ve seen the technical definitions. Now here’s a broader perspective on why “good” isn’t just a number.

Most credit content focuses on hitting a specific score threshold as if crossing 670 or 700 is the finish line. It isn’t. What most guides fail to emphasize is that the same score means different things depending on the context, the scoring model in use, and the specific lender’s internal criteria. A 695 might get you approved at one bank and declined at another because lenders layer their own risk models on top of the public scoring models.

The 30 to 50 point difference between FICO and VantageScore isn’t a glitch. It reflects two genuinely different philosophies about what makes someone a good credit risk. Chasing a specific number without knowing which model matters for your goal is like training for the wrong race.

Here’s what we consistently see at Credit Rebooter: people obsess over the exact cutoff while ignoring the broader habits that drive all score models upward. Paying every bill on time, keeping balances low, and avoiding unnecessary new accounts will improve your score under every model, in every version, with every lender. Those habits are model-agnostic.

The smarter approach is to understand your credit score explanation as a snapshot of your financial habits rather than an end goal. Progress beats perfection. Someone who moves from 580 to 650 in six months and continues on an upward trajectory is in a far better position than someone stuck at 700 who doesn’t understand why it won’t move higher.

Focus on the behaviors, not the badge. Know which model your lender checks. Understand your full profile, not just the headline number. That combination of awareness and consistent positive action is what produces lasting financial opportunity.

Take your next steps to better credit

Ready to put this knowledge into practice? Here’s how you can move from learning to action.

Understanding what makes a good credit score is only valuable if you act on it. Whether you’re an individual working toward a mortgage or a small business owner trying to secure your first line of credit, the path forward starts with an honest look at where your score stands today and what’s holding it back.

Credit Rebooter’s credit score repair resources give you a structured process to identify and address the specific items dragging your score down, from late payments to high utilization to outdated negative marks. For those ready to build rather than just repair, our credit building strategies guide walks you through proven steps to grow your score consistently over time. You don’t have to guess at what works. We’ve mapped the path, and you can start walking it today.

Frequently asked questions

Can I improve my credit score quickly?

Some improvements can appear within one to three months by paying down high credit card balances, making on-time payments, and disputing inaccurate items on your credit report.

Which is more important, my FICO or VantageScore?

Most lenders use FICO for major credit decisions, as FICO dominates 90% of lenders, but monitoring both scores helps you spot potential issues and prepare for applications where VantageScore may be used.

How long does negative information stay on my credit report?

Most negative marks stay on your report for seven years, though newer scoring models ignore paid collections, meaning a settled debt may no longer affect your score under more current versions.

Is my business credit score different from my personal score?

Yes, business credit is tracked separately, but most small business loans still require a solid personal credit score, especially for businesses with fewer than two to three years of credit history.

Does checking my own credit score hurt my score?

No. Checking your own credit is a soft inquiry, which means it has zero impact on your score regardless of how often you check it.