Most people assume credit bureaus hold the keys to their financial future, that these agencies decide who gets a loan and who gets rejected. That belief is wrong, and it costs people real money. Credit bureaus are data suppliers, not decision makers. The moment you understand that distinction, everything about improving your credit score becomes clearer and more actionable. In this article, we break down exactly how credit bureaus operate, how your data gets collected, how scores are calculated, and what you can do right now to put yourself in a stronger financial position.

Table of Contents

- What is a credit bureau?

- The major credit bureaus: Equifax, Experian, TransUnion

- How credit bureaus collect and use your data

- How credit scores are calculated: FICO vs. VantageScore

- Business credit bureaus and building business credit

- The uncomfortable truth: Credit bureau errors are more common than you think

- Next steps: Take control with expert credit repair

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Bureaus collect credit data | Credit bureaus gather and organize information from lenders to create your credit report. |

| Scores vary by bureau | Your credit score can differ depending on which bureau’s data a lender pulls. |

| Dispute errors quickly | Promptly check all reports and dispute any inaccuracies to protect your financial status. |

| Business credit is separate | Small businesses should build distinct credit profiles through dedicated bureaus and trade lines. |

| Credit improvement is actionable | Pay on time, manage balances, and monitor your reports to boost your credit score fast. |

What is a credit bureau?

A credit bureau is a private company that gathers, organizes, and stores financial information about you. Think of it as a filing clerk that keeps records of your borrowing behavior but never actually grades your application. Credit bureaus collect and organize information from lenders, landlords, and public records, then package it into a credit report that other companies can purchase.

Here is what credit bureaus actually do:

- Collect payment history, balances, and account details from lenders

- Record bankruptcies and certain public records

- Generate credit reports for authorized requesters

- Support lenders, landlords, and employers with data for their own decisions

- Maintain dispute resolution processes for inaccurate data

Bureaus do not decide loans or set your interest rate. That part is entirely up to the lender. Bureaus are governed by the Fair Credit Reporting Act (FCRA), a federal law that regulates how consumer data is collected, stored, and shared. The FCRA gives you specific rights, including the right to see your own report and dispute errors.

Understanding your credit reports and scores is the first practical step toward taking control of your financial profile. Knowing what information goes in means you know exactly what to fix. If you want to explore your rights and obligations under federal law, our regulatory disclosure page is a useful starting point.

For context, people who work in credit analyst roles spend their careers interpreting the data bureaus produce. Even they will tell you the bureau just provides the raw material. The lender cooks the meal.

The major credit bureaus: Equifax, Experian, TransUnion

There are three major credit bureaus in the United States, and each one operates independently. That independence is actually one of the most misunderstood aspects of credit reporting.

| Bureau | Founded | Headquarters | Coverage |

|---|---|---|---|

| Equifax | 1899 | Atlanta, GA | 800M+ consumers globally |

| Experian | 1996 (U.S.) | Dublin, Ireland | 1B+ records globally |

| TransUnion | 1968 | Chicago, IL | 500M+ consumers globally |

The three major U.S. credit bureaus each collect data independently, which means they may not have identical information on file for you. One lender might report to Experian but not TransUnion. Another might report to all three. This creates a situation where your credit score can differ depending on which bureau a lender pulls.

“Scores differ across bureaus due to data variances; lenders may pull one, so monitor all three.”

That is not a glitch. It is how the system is built. A mortgage lender might pull all three and use the middle score. An auto dealer might only pull one. You have no way of knowing which bureau a lender will check, which is exactly why monitoring your credit score ratings at all three bureaus matters so much.

Equifax is one of the oldest, with roots going back to a grocery store that tracked who paid their bills on time. Experian grew quickly through acquisitions and now serves as a major global player. TransUnion started in the railroad industry and evolved into a consumer credit powerhouse. All three are private companies, not government agencies, though they are heavily regulated.

How credit bureaus collect and use your data

Data is the raw material that powers your credit report. Knowing where it comes from gives you the ability to catch mistakes before they cost you.

Bureaus pull from two main source types. First are furnishers: banks, credit card companies, auto lenders, mortgage servicers, and student loan providers. Second are public records, primarily bankruptcy filings. Data sources include banks and public records such as bankruptcies. Notably, tax liens and civil judgments were removed from credit reports in 2017 and are no longer included.

Here is what typically appears on a credit report:

- Payment history (on time, late, missed)

- Account balances and credit limits

- Account age and type

- Hard inquiries from credit applications

- Bankruptcy filings

Here is what does NOT appear:

- Income or employment history

- Tax liens (removed since 2017)

- Civil court judgments

- Bank account balances

Negative information stays for 7 years on your report, while a Chapter 7 bankruptcy remains for 10 years. More concerning, the FTC found that 1 in 5 consumers has a material error on at least one report.

Pro Tip: Visit AnnualCreditReport.com weekly (now permanently free under FCRA rules) and pull reports from all three bureaus. If you spot an error, follow the credit report error steps immediately. The CFPB guide also outlines your rights during disputes. Errors that affect your score can be corrected, but only if you catch them. For a broader foundation, our credit essentials resource covers the full picture.

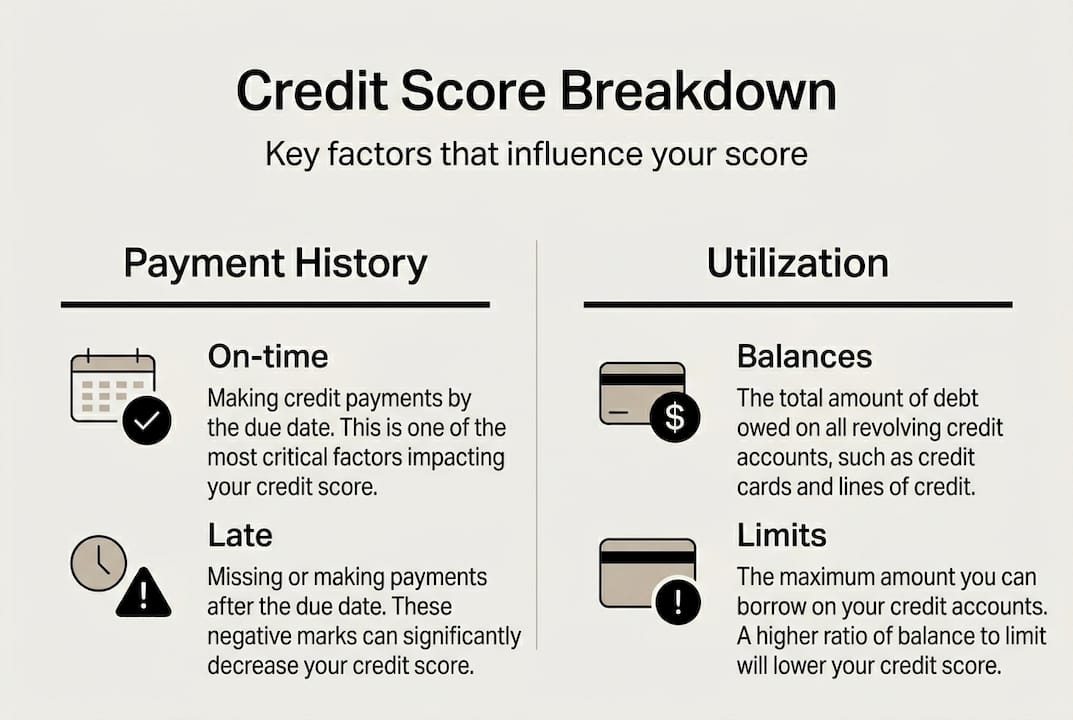

How credit scores are calculated: FICO vs. VantageScore

Your credit report is the raw data. Your credit score is what lenders actually see at a glance. Two major models convert that data into a number between 300 and 850.

FICO score weighting:

- Payment history: ~35%

- Amounts owed (utilization): ~30%

- Length of credit history: ~15%

- New credit (inquiries): ~10%

- Credit mix: ~10%

VantageScore weighting:

- Payment history: ~41%

- Depth of credit: ~20%

- Credit utilization: ~20%

- Balances: ~11%

- Recent credit and available credit: ~8%

Credit scores are derived using these weighted factors, which is why improving payment history and reducing your balance have the fastest impact on your score.

Stat: FICO is used by 90% of top lenders, making it the dominant model in lending decisions. VantageScore, however, scores roughly 33 million more consumers because it can generate a score with as little as one month of credit history. This makes it valuable for people who are new to credit.

Newer versions of both models reward steady paydown of revolving balances. That means consistently lowering your credit card balances, even gradually, moves the needle more than many people expect.

Pro Tip: Focus your energy on payment history and utilization first. Those two factors alone control about 65% of your FICO score. Explore credit score repair strategies designed around exactly these priorities.

Business credit bureaus and building business credit

If you run a small business, your personal credit is not the only score that matters. Business credit operates through a completely separate system with its own bureaus and scoring models.

The three major business credit bureaus are:

- Dun & Bradstreet: Uses the PAYDEX score (0 to 100), which measures how promptly a business pays its bills

- Experian Business: Uses the Intelliscore Plus (1 to 100)

- Equifax Business: Tracks payment trends and credit risk for commercial accounts

For small businesses, separate bureaus track trade payments, and personal credit is commonly checked for startups that lack a business credit history.

Here is the important distinction: your business credit and personal credit are legally separate once you set them up correctly. That separation protects your personal score from business setbacks and unlocks larger credit lines for your company.

How to start building business credit:

- Register your business and obtain an EIN (Employer Identification Number)

- Open a dedicated business checking account

- Apply for a business credit card or net-30 vendor account

- Work with suppliers who report payments to business bureaus

- Monitor your business reports regularly

Pro Tip: Start building your business credit history the moment you register your business, even if you do not need a loan yet. Early trade lines create the history that makes future financing much easier. Learn more about building business credit through structured steps, or explore how business lines of credit can accelerate your growth.

The uncomfortable truth: Credit bureau errors are more common than you think

Most articles about credit bureaus treat them as reliable systems that occasionally slip up. Here is our honest take: the data sitting inside these bureaus may be wrong right now, and you probably have not checked.

The FTC confirmed that 1 in 5 reports have errors significant enough to affect a consumer’s score. That is not a rounding error in the system. That is a systemic problem affecting tens of millions of people. What makes it worse is that most consumers never look at their reports until they are denied for something important.

Conventional advice says to check your credit once a year. We think that is outdated. With free weekly access now permanent, there is no reason to wait. The credit bureau system depends on furnishers reporting accurate data, but furnishers make mistakes constantly. Accounts get misreported. Old collections reappear. Identity theft introduces fraudulent accounts.

Actively protecting your credit profile means treating it like your bank account, something you review regularly, not just when something feels off. The moment you spot something wrong, follow the fixing report errors process. Bureaus are required to investigate disputes within 30 days. That is your right, and it works when you use it consistently.

Next steps: Take control with expert credit repair

Now that you understand how credit bureaus actually work, you can stop guessing and start acting. Knowledge without a plan only gets you so far.

At Credit Rebooter, we turn your understanding into real results. Whether you need to dispute errors, build a stronger history, or design a plan to hit your target score, we have the tools and guidance to get you there. Explore credit building strategies tailored to your situation, check out our credit score repair services to fast-track your progress, or start with our resources on how to improve your credit history step by step. Your credit profile is not fixed. It is a work in progress, and we are here to help you build it right.

Frequently asked questions

How do I check my credit report for free?

You can access your free weekly credit reports from each bureau through AnnualCreditReport.com as permanently mandated by the FCRA. Pull all three bureaus to get the full picture.

How long do negative credit items stay on my report?

Most negative marks remain for 7 years, while a Chapter 7 bankruptcy stays on your report for 10 years from the filing date.

What should I do if I find an error on my credit report?

Dispute the error directly with the credit bureau or the data provider. Under the FCRA, they must investigate within 30 days and correct or remove anything they cannot verify.

Do credit bureaus decide whether I get a loan or set my interest rate?

No. Bureaus provide neutral data to lenders, but approval decisions and interest rates are set entirely by the lender based on their own criteria.

Can I improve my credit score quickly?

The fastest results come from paying every bill on time, keeping your utilization below 30%, and disputing any errors on all three of your credit reports right away.