The average credit score for white Americans sits around 719, while Black Americans average 621. That nearly 100-point gap can mean the difference between a mortgage approval and a rejection, a low interest rate and a punishing one, or a business loan and a dead end. Your credit score disparities affect your financial life more than almost any other number. Whether you want to buy a home, finance a car, or qualify for a business line of credit, this article breaks down exactly what a credit score is, what drives it, and what you can do about it starting today.

Table of Contents

- What is a credit score?

- What affects your credit score: Key factors explained

- How to read a credit report and spot problems

- Actionable steps to improve your credit score

- Why credit score advice often misses the mark

- Get expert help improving your credit score

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Credit score basics | Your credit score is a three-digit number that lenders use to quickly gauge your ability to repay debts. |

| Biggest score factors | Payment history and debt utilization have the largest impact on your score. |

| Small changes matter | Lowering credit card balances can boost your score significantly in as little as one month. |

| Disparities persist | There are persistent gaps in credit scores across race and class, even when habits are similar. |

| Actionable improvements | Regularly check your report and use proven steps to improve your score over time. |

What is a credit score?

A credit score is a three-digit number, typically ranging from 300 to 850, that tells lenders how likely you are to repay a debt. Think of it like a report card for your financial behavior. The higher the number, the better you look to anyone deciding whether to lend you money, rent you an apartment, or in some cases, hire you for a job.

Two scoring models dominate the market:

- FICO Score: The most widely used model, developed by the Fair Isaac Corporation. Most lenders rely on it when you apply for a mortgage or auto loan.

- VantageScore: A competing model created by the three major credit bureaus. It uses similar criteria but can score people with shorter credit histories.

Both models use the same basic scale, but the weights they give each factor differ slightly. Knowing which model a lender uses can actually change how you prioritize your credit-building moves.

Lenders are the obvious users of your score, but landlords often check it before approving a lease, and some employers pull it during background screening for finance-related roles. For small business owners, this gets especially important. Most small business lenders check your personal credit score before approving a business loan, particularly if your business is young and lacks a separate credit history. A weak personal score can close doors before you even start the conversation.

Learn the credit score basics to understand which model applies in your situation.

“A strong credit score is not just a financial metric. It is a gateway to opportunity, and the gap between groups is wide enough to change life outcomes.”

Research shows that scores rise with age, but demographic gaps persist across income and racial lines, making it critical that everyone understands their score and how to move it forward.

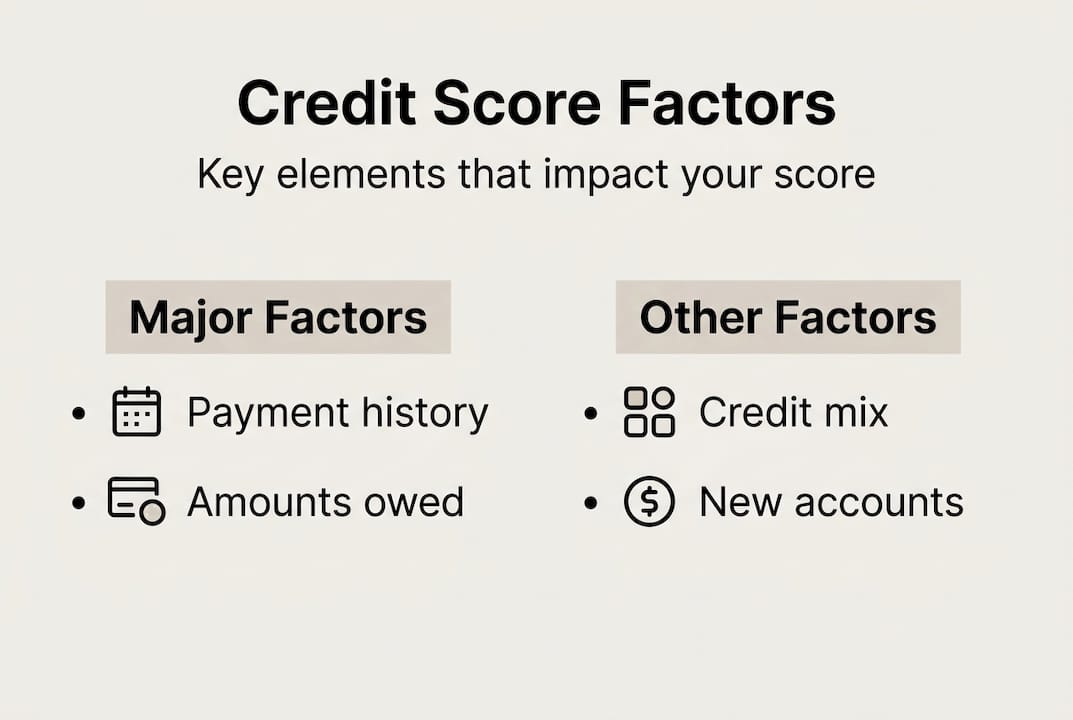

What affects your credit score: Key factors explained

Your credit score is not random. Five specific factors shape it, and each one carries a different weight. Here is a quick look at what matters most:

| Factor | Weight (FICO) | What it measures |

|---|---|---|

| Payment history | 35% | On-time vs. late payments |

| Amounts owed | 30% | Credit utilization ratio |

| Length of credit history | 15% | Age of your oldest and newest accounts |

| New credit | 10% | Recent hard inquiries and new accounts |

| Credit mix | 10% | Variety of account types |

Payment history is the single biggest factor. One missed payment can drop your score significantly, especially if it goes 30 or more days past due. Amounts owed, often called credit utilization, measures how much of your available credit you are actually using. Staying below 30% is the general recommendation, but below 10% is even better.

Here is a real example of how powerful utilization can be: a utilization drop from 76% to 4% on a single card boosted a FICO score by 37 points. That is a significant jump without changing any other behavior.

Here are practical steps to control each factor:

- Set up autopay to protect your payment history.

- Pay down balances before your statement closing date to reduce reported utilization.

- Keep old accounts open even if you rarely use them, to protect your history length.

- Limit applications for new credit to avoid unnecessary hard inquiries.

- Over time, add a mix of credit types, such as a credit card plus an installment loan.

Pro Tip: If you have one high-balance card, pay it down first before spreading payments across multiple cards. Dropping one card’s utilization dramatically has a faster effect than making tiny payments everywhere.

For a deeper guide on improving your credit score, explore strategies tailored to your specific situation.

How to read a credit report and spot problems

Your credit score is calculated from data in your credit report. The report and the score are two different things. The report is the full file; the score is the summary number. Understanding what’s inside the report helps you catch errors before they cost you.

A standard credit report has four main sections:

| Section | What it contains |

|---|---|

| Personal information | Name, address, Social Security number, employment history |

| Account history | Credit cards, loans, payment records, balances |

| Inquiries | Hard and soft pulls on your credit |

| Public records | Bankruptcies, collections, civil judgments |

Common errors that hurt your score include:

- Accounts that do not belong to you (possible identity theft or mixed files)

- Incorrect late payment records

- Balances that have not been updated after payoff

- Duplicate accounts listed more than once

- Wrong personal information tied to someone else’s file

Errors and inaccuracies can impact score outcomes across demographics, and they are more common than most people expect. You have the legal right to dispute any error with the credit bureau that reported it.

To dispute an error, gather supporting documents, write a clear dispute letter explaining the problem, and submit it to the relevant bureau online or by mail. Bureaus have 30 days to investigate. If the item is not verified, they must remove it.

Pro Tip: Pull your report from all three bureaus, Equifax, Experian, and TransUnion, at least once a year. Errors can appear at one bureau but not the others, and each bureau’s data may differ.

If you need guidance on fixing credit report errors, step-by-step resources are available to help you navigate the dispute process without frustration.

Actionable steps to improve your credit score

Knowing what affects your score is one thing. Doing something about it is another. Here is a clear action plan you can start using right now.

- Pay every bill on time. Set reminders or autopay for every account. Even one 30-day late payment can drop your score significantly.

- Lower your credit utilization. Aim to use less than 30% of each card’s limit. Pay down balances before your statement date so a lower number gets reported.

- Dispute errors immediately. Review your report and file disputes for anything inaccurate. Removing a wrong late payment or incorrect collection account can move your score fast.

- Avoid opening new accounts you do not need. Every hard inquiry from a new application can chip away at your score, especially if done frequently.

- Keep old accounts open. Length of history matters, so closing an old account can actually hurt you.

For small business owners, a few extra considerations apply:

- Keep personal and business spending on separate cards to monitor each clearly.

- Pay down personal cards aggressively before applying for a business loan.

- Consider secured business credit cards to build a business credit profile without relying entirely on personal credit.

A utilization drop from 76% to 4% produced a 37-point FICO gain, which shows that even targeted action on one account can create real movement.

Pro Tip: If you are carrying a large balance on one card, try making a payment mid-cycle before the statement closes. Your reported balance drops, and your score can improve within one billing cycle.

For more detailed credit improvement tips or a full roadmap to raising your credit score, you will find targeted strategies to match your starting point.

Why credit score advice often misses the mark

Most credit advice sounds like this: pay your bills on time, keep your balances low, do not apply for too much credit. It is all technically correct. But it treats everyone as if they are starting from the same place, and that is where it falls apart.

The reality is that gaps by race and class persist even as credit scores rise with age, pointing to structural barriers that generic tips simply cannot fix. If you grew up in a household without access to traditional banking, or if your family’s financial history limited your early credit access, “just pay on time” is not actionable advice. You need a plan that accounts for where you actually are.

What works better is a systematic, personalized approach: audit your current report, identify the one or two factors dragging your score down the most, and attack those specifically. Quick hacks like adding yourself as an authorized user on a family member’s account can help, but they are a bridge, not a destination.

Patience also matters more than most people want to hear. Credit improvement is measured in months, not days. But steady, consistent action on the factors within your control compounds over time. For effective credit score improvement, the most important thing is to start with an honest look at your report and build a plan from there, not from someone else’s starting line.

Get expert help improving your credit score

Understanding your credit score is a great first step. Acting on it with the right support is what actually changes the number.

At Credit Rebooter, we offer credit score repair services designed for real people dealing with real financial situations, not one-size-fits-all templates. Whether you are recovering from late payments, dealing with errors on your report, or starting to build credit from scratch, our credit building strategies give you a personalized path forward. If your score is in rough shape, our bad credit solutions can help you stabilize and rebuild faster than going it alone. Reach out today and let us help you build the credit foundation your financial goals deserve.

Frequently asked questions

What is a good credit score in the U.S.?

In most models, a score of 670 or above is considered good, 740 or above is very good, and 800 or above is excellent. These credit score ranges directly affect the interest rates and terms you can qualify for.

How quickly can I improve my credit score?

You may see improvement within one billing cycle if you lower your credit utilization, but sustained changes like building a longer payment history take several months to show significant results.

Does checking my credit score hurt my credit?

No, checking your own score is a soft inquiry and does not affect your credit score at all. Only hard inquiries triggered by credit applications can have an impact.

Why do credit scores vary among different groups?

Scores differ because of persistent demographic gaps tied to historical and structural inequalities in access to banking, credit, and financial education across race and income lines.

Can small business owners use business credit instead of personal credit?

Most lenders review both, so a strong personal credit score remains very important for small business financing, especially when your business is less than two years old.