Your credit score is quietly shaping some of the biggest decisions of your life. A low score can block you from getting a mortgage, force you into sky-high auto loan rates, or get your rental application rejected. The frustrating part? Most people don’t realize how close they are to a real breakthrough. With the right actions in the right order, improving your credit score is not a years-long slog. It’s a structured process with predictable results. This guide walks you through exactly what to do, step by step, so you can hit the numbers that unlock the financial goals you’ve been working toward.

Table of Contents

- Understanding how credit scores work

- Step 1: Pay bills on time, every time

- Step 2: Slash your credit utilization

- Step 3: Strengthen your credit history and mix

- Step 4: Dispute errors and leverage new reporting tools

- Our take: What most miss about raising your credit score

- Take your next step with expert credit support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| On-time payments matter | Making every payment on time has the largest single effect on your score. |

| Credit utilization is key | Aim to keep credit utilization below 10% for a fast, significant boost. |

| Dispute errors monthly | Regularly check and fix report errors to recover lost points and avoid surprises. |

| Old accounts help | Keep old credit lines open to maximize your history and mix. |

Understanding how credit scores work

Before you can change your score, you need to know what’s actually driving it. Two models dominate the credit scoring world: FICO and VantageScore. Lenders, banks, and car dealerships almost universally use one of these two to evaluate your creditworthiness. Both models look at the same core data from your credit reports, but they weigh things slightly differently.

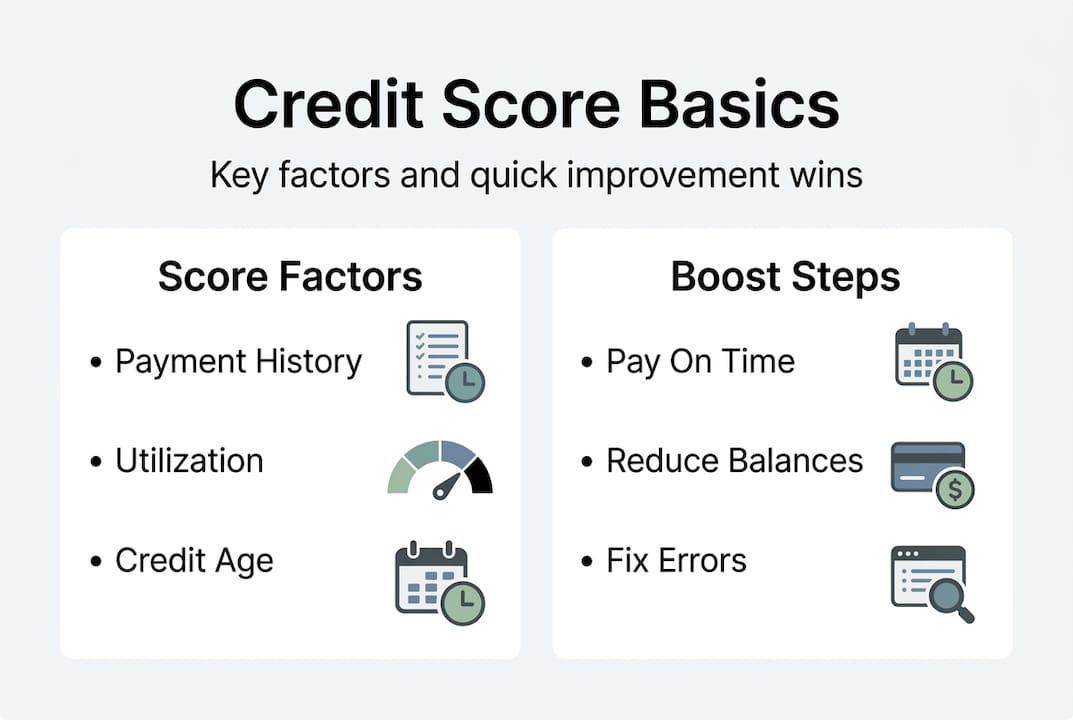

Here’s how FICO breaks down the five key factors:

| Factor | Weight |

|---|---|

| Payment history | 35% |

| Amounts owed (utilization) | 30% |

| Length of credit history | 15% |

| New credit | 10% |

| Credit mix | 10% |

As you can see, payment history accounts for 35% of your FICO score, making it the single biggest lever you can pull. Amounts owed comes in second at 30%, which is why carrying high balances can crush your score even when you’re paying every bill on time.

Where do you stand compared to other Americans? The average FICO score is 715, with 670 or above considered good and 740 or above considered excellent. Crossing that 740 threshold is often where the real rewards kick in: better mortgage rates, lower car loan interest, and premium credit card approvals.

Why does this matter so much for a home or car purchase? A difference of just 50 points can mean thousands of dollars in extra interest over the life of a loan. Lenders don’t just use your score to say yes or no. They use it to decide what rate to charge you. That’s why understanding credit scores explained by federal resources is a smart starting point.

Here are the score ranges to keep in mind:

- Exceptional: 800 and above

- Very good: 740 to 799

- Good: 670 to 739

- Fair: 580 to 669

- Poor: Below 580

If you’re in the fair or poor range, don’t be discouraged. The factors are knowable, and the fixes are learnable. Check out these improving credit score tips and get a head start on your plan.

Pro Tip: Don’t obsess over getting to 850. Getting from 620 to 740 will unlock nearly the same loan terms as a perfect score. Focus on crossing the next tier, not chasing perfection.

Step 1: Pay bills on time, every time

Now that you know payment history is king, here’s how to make sure you always pay on time.

One missed payment can do serious damage fast. A 30-day late payment can drop a score of 780 by 90 to 110 points. That’s not a typo. A single slip, on a single account, can cost you more than a hundred points overnight. And because payment history makes up 35% of your FICO score, no other action will give you a bigger return than simply paying on time.

The good news is this factor is almost entirely within your control. Here’s how to build a system so you never miss:

- Set up autopay. Turn on automatic minimum payments for every account. Even if you plan to pay more, this guarantees you won’t miss a due date.

- Create calendar reminders. For bills that don’t offer autopay, set a recurring monthly alarm three to five days before the due date.

- Consolidate due dates. Call your lenders and ask to move your due dates to around the same time each month. This simplifies tracking.

- Prioritize credit card and loan payments first. Utilities and subscriptions rarely report to credit bureaus until you’re very late. Credit accounts report at 30 days.

- Address missed payments immediately. If you’ve already missed one, pay as soon as possible. The damage worsens at 60 and 90 days, so getting current quickly limits the fallout.

If you have old late payments on your report, you can sometimes request a “goodwill adjustment” from the lender, especially if your payment record has been clean since then. It doesn’t always work, but it costs you nothing to ask.

One more important point: paying the minimum is enough to protect your payment history. You don’t need to pay in full every month to avoid a negative mark. Full payment helps your utilization, but on-time payment protects your history. Use this credit score improvement guide to build a payment plan that works with your budget.

Pro Tip: If cash is tight, always protect your credit card and loan payments first. A missed credit payment shows up on your credit report. A missed Netflix payment usually doesn’t.

Step 2: Slash your credit utilization

With your payment schedule rock solid, the next fastest win is cutting your credit utilization.

Credit utilization is simply how much of your available credit limit you’re currently using. If you have a $10,000 limit and carry a $4,000 balance, your utilization is 40%. Utilization makes up 30% of your FICO score, and the best scorers in the country average just 7%.

Here’s why this matters so much: utilization is recalculated every month when your lender reports your balance to the bureaus. That means dropping your balance can improve your score within a single billing cycle. It’s one of the fastest adjustments you can make.

| Utilization Rate | Score Impact |

|---|---|

| Under 10% | Excellent |

| 10% to 30% | Good |

| 30% to 50% | Moderate negative |

| Over 50% | Strong negative |

Here’s what to focus on:

- Pay down balances aggressively. Target your highest utilization cards first, even if they aren’t your highest interest cards.

- Ask for a credit limit increase. If your income has grown, call your card issuer and request a higher limit. This instantly lowers your utilization without changing your balance.

- Make multiple payments per month. Paying twice a month keeps your reported balance lower even if you spend regularly.

- Don’t close old cards. Closing a card reduces your total available credit, which spikes your utilization immediately.

One counterintuitive insight: spreading balances across multiple cards is worse than concentrating them on one card near zero and one card partially used. Aim to get as many accounts as possible to zero, even if one card carries a small remaining balance.

For a full breakdown of the best approach to building credit strategies, explore our resources on improving your credit score with proven balance management methods.

Pro Tip: Ask your card issuer when they report your balance to the bureaus. Paying down before that date, not just before the due date, can make a meaningful difference in what score a lender sees.

Step 3: Strengthen your credit history and mix

Beyond payments and balances, your score is also shaped by the age and variety of your credit.

Credit history length counts for 15%, new credit 10%, and mix 10% of your FICO score. Together, these three factors make up 35% of your total score. That’s equal to payment history, so they deserve real attention.

Here’s what you need to know:

- Keep old accounts open. The age of your oldest account, your newest account, and the average age of all accounts all factor into your score. Closing old cards drops your average age and can hurt significantly.

- Don’t open accounts you don’t need. Every new account application triggers a hard inquiry, which can drop your score by five to ten points. Multiple inquiries in a short window look risky to lenders.

- Diversify your credit mix intentionally. Having both revolving credit (cards) and installment loans (auto, student, personal) shows lenders you can handle different types of debt.

- Consider a credit builder loan. These small loans, offered by many credit unions, are designed specifically to add an installment account to your profile without much risk.

The single best thing you can do for your credit history is nothing. Keep old accounts open, use them occasionally, and let time do the work.

For a deeper look at factors affecting your credit score, Experian’s breakdown is worth reading. And if you’re still building credit history from scratch, there are structured approaches that can fast-track your timeline. Visit our credit building tips page for a personalized starting point.

Step 4: Dispute errors and leverage new reporting tools

Solid habits matter, but so does keeping your records error-free and using every advantage available.

26% of credit reports contain errors, and some of those errors are serious enough to tank a score by dozens of points. That means one in four people reading this likely has inaccurate information dragging their score down right now.

Here’s how to dispute errors step by step:

- Pull your free report from all three bureaus at AnnualCreditReport.com.

- Review each report for accounts you don’t recognize, incorrect late payments, wrong balances, or outdated negative items.

- File a dispute directly with the bureau reporting the error online, by mail, or by phone.

- Include documentation, such as bank statements or payment confirmations, to support your case.

- The bureau has 30 days to investigate and must remove unverified items.

Beyond fixing errors, new tools can add positive data directly to your report:

- Experian Boost: Links your bank account and adds on-time utility, streaming, and rent payments to your Experian report for an instant score increase.

- FICO 10T and VantageScore 4.0 use trended data, which looks at your balance patterns over time rather than just a single snapshot. They’re also less punitive on medical debt and now include rent and utility payments in scoring calculations.

You can check your credit report for free every week at AnnualCreditReport.com. Use that access to monitor changes and catch problems early. For help navigating the dispute process, our guides on steps to credit repair, credit score repair, and understanding credit files walk you through every stage.

Our take: What most miss about raising your credit score

Here’s the bigger picture our team wants you to hold onto.

Most people approach credit repair looking for a shortcut. They close old cards to feel organized. They pay off an ancient collection account expecting an instant boost. They apply for a balance transfer card thinking it will solve everything. These moves often backfire because they ignore how scoring models actually respond to change.

The real lever isn’t any single action. It’s systemizing your habits so that the right signals flow to your report automatically every month. Autopay, controlled utilization, and a hands-off approach to old accounts will outperform any clever trick over a six to twelve month window.

Scoring models are also evolving in ways most people, and even some financial advisors, don’t fully appreciate. FICO 10T rewards those who consistently reduce balances over time, not just those who carry low balances once. That shift rewards discipline, not just a single good month.

We’ve seen people go from a 580 to a 720 in under a year simply by automating payments and getting off the balance treadmill. No gimmicks. No risky moves. Just consistent behavior rewarded by a system built to measure exactly that. Start with our guide on raising your credit score and build on a foundation that actually lasts through building credit repair strategies designed for real results.

Take your next step with expert credit support

Ready to make your efforts count? Here’s the easiest way to accelerate your credit journey.

Knowing what to do is powerful. Getting it done consistently is where most people need support. Credit Rebooter offers both the tools and the guidance to help you move from where you are now to where you need to be for that home purchase, car loan, or business funding.

Explore our personalized credit strategies to build a plan tailored to your situation. If your report has errors or negative items dragging you down, our credit score repair services can help you address them efficiently. And if you’re ready to see real numbers move, start with our step-by-step plan to increase your credit score and track your progress week by week.

Frequently asked questions

How quickly can I increase my credit score?

With the right steps, improvements can arrive in as little as 30 days. Reducing high utilization can add 20 to 40 or more points in a single billing cycle.

Does checking my own credit hurt my score?

No. Checking your own report is a soft inquiry and has zero effect on your score. Your own inquiries are completely excluded from scoring calculations.

Should I close unused credit cards to improve my score?

Generally, no. Closing cards can spike your utilization rate and shorten your average credit history, both of which lower your score.

What’s the fastest route to an excellent (740+) credit score?

Pay every bill on time, keep utilization under 10%, and dispute any errors on your reports. Reaching the 740+ range qualifies you for the best available rates on mortgages and auto loans.

Recommended

- How To Improve Your Credit Score | Credit Rebooter

- 101 Useful Improving Your Credit Score | Credit Rebooter

- Tips On How To Improve Your Credit Score | Credit Rebooter

- Improve You Credit Score | Credit Rebooter

- Fix Credit Before Buying Home NZ: Boost Score 50% in 6 Months

- Credit Scores for Mortgages: 50-Point Boost Saves Thousands