Many Americans assume all three credit bureaus hold identical information about them. That assumption can cost you real money. Your credit reports can differ widely across Equifax, Experian, and TransUnion, as reports vary by bureau, which means a score you check in one place might look very different somewhere else. Whether you are an individual trying to qualify for a mortgage or a small business owner seeking a line of credit, understanding how credit agencies actually work puts you in control. This article breaks down the roles these agencies play, how they calculate your score, common pitfalls to avoid, and what small business owners need to know to build strong credit from the ground up.

Table of Contents

- What are credit agencies and why do they matter?

- How credit agencies calculate your score

- Common credit reporting pitfalls and how to avoid them

- The special role of credit agencies for small business owners

- Why viewing credit agencies as ‘the enemy’ misses the mark

- Take the next step to improve your credit

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Three bureaus, different data | Experian, Equifax, and TransUnion each collect slightly different information and may offer unique scores for the same person. |

| Scores reflect multiple factors | Your payment history, utilization, and credit mix make up most of your score in common models. |

| Spot and fix credit errors | Review all your reports and dispute mistakes quickly to protect and improve your score. |

| Small business credit starts personal | A strong personal credit score often unlocks business financing before a separate business profile is established. |

What are credit agencies and why do they matter?

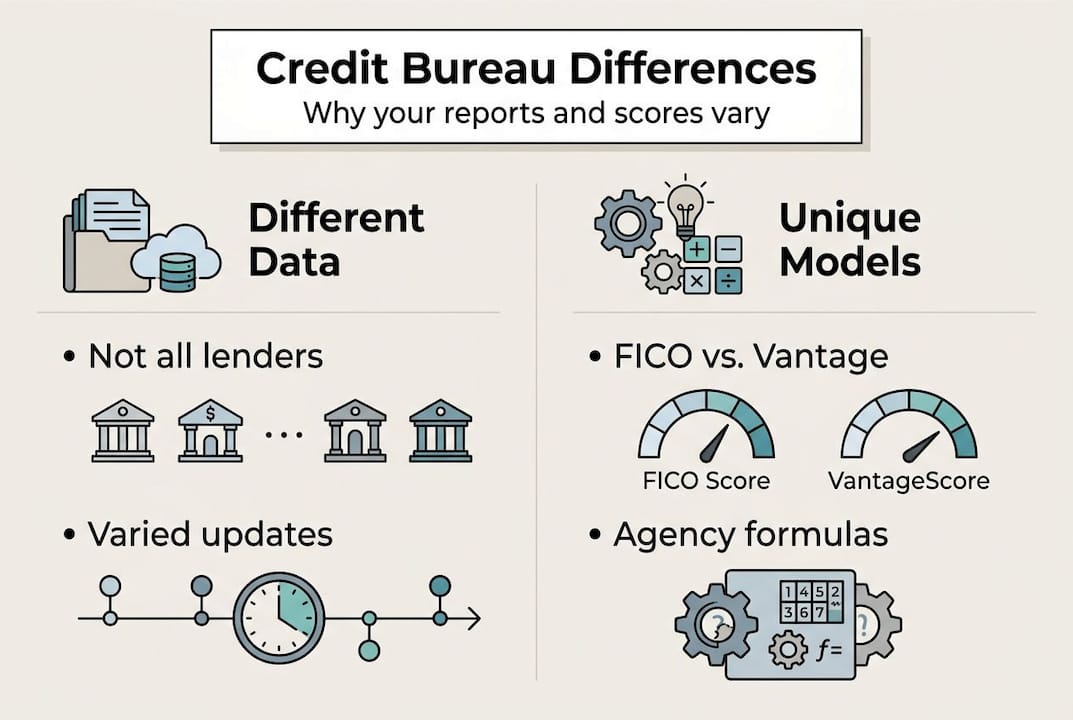

Credit agencies, also called credit bureaus, are private companies that collect and store financial data about you. They gather information from lenders, credit card companies, and other creditors, then compile it into reports that banks and businesses use to judge your creditworthiness. Three major bureaus dominate the U.S. market: Equifax, Experian, and TransUnion. Each one operates independently, which means the data they hold about you is not always the same.

Here is what each bureau typically collects:

- Payment history on loans and credit cards

- Current balances and credit limits

- Length of time accounts have been open

- Public records such as bankruptcies or judgments

- Hard inquiries from lenders when you apply for credit

For individuals, this data shapes whether you get approved for a car loan, an apartment, or a home mortgage. For small business owners, your personal credit reports and scores often serve as the first indicator of your financial reliability before a true business profile exists.

Why do reports differ? Because not all lenders report to all bureaus. A credit card company might send data only to Experian, while your auto lender reports to all three. This creates gaps, which is why your score at one bureau might be 30 or 40 points higher than at another.

| Bureau | Common data focus | Business credit products |

|---|---|---|

| Equifax | Employment history, personal data | Equifax Business Credit |

| Experian | Trade lines, collections | Experian Business Credit |

| TransUnion | Fraud signals, inquiries | TransUnion Business |

Understanding what a credit report score means at each bureau is the foundation of taking real control over your financial life.

Pro Tip: Pull all three of your credit reports at annualcreditreport.com every year. Compare them side by side to catch accounts that appear on one report but not another, which can signal data errors or even identity theft.

How credit agencies calculate your score

With the basics covered, it is time to see exactly how these agencies calculate and sometimes differ on your score.

There are two scoring models you will hear about most often: FICO and VantageScore. Both run on a scale of 300 to 850, and both use similar data, but they weight factors differently. FICO and VantageScore differ in how they prioritize payment history, credit utilization, account age, and new credit inquiries.

Here is a side-by-side comparison of the two models:

| Factor | FICO weight | VantageScore weight |

|---|---|---|

| Payment history | 35% | Extremely influential |

| Credit utilization | 30% | Highly influential |

| Length of credit history | 15% | Moderately influential |

| Credit mix | 10% | Less influential |

| New credit inquiries | 10% | Less influential |

The numbered breakdown below shows how your everyday behaviors feed into your credit score factors:

- Pay on time, every time. A single missed payment over 30 days late can drop a strong score by 80 to 110 points almost overnight.

- Keep utilization below 30%. Using more than 30% of your available credit signals risk to lenders, even if you pay in full monthly.

- Keep old accounts open. Closing a long-standing account shortens your average account age and can lower your score.

- Limit new applications. Each hard inquiry from a new application stays on your report for two years.

- Maintain a mix of credit types. Having both revolving credit (cards) and installment loans (car, mortgage) looks more stable to scoring models.

Scores update as new data arrives from lenders, usually monthly. That means a positive change like paying down a large balance can show up quickly. For a deeper breakdown of all the moving parts, reviewing your credit score details is a smart next move.

Statistic callout: One missed payment can reduce a score of 780 or higher by as much as 110 points, while the same missed payment on a 680 score might drop it by about 60 to 80 points. The higher your score, the more you have to lose.

Common credit reporting pitfalls and how to avoid them

Understanding the formulas is just one piece. Real-life mistakes and errors can trip anyone up, often without warning.

The most damaging events to your credit include:

- Late payments: Even one payment over 30 days late gets reported and can stay for seven years

- High utilization: Pushing balances close to your credit limits signals financial stress

- Collections accounts: Unpaid debts sent to collectors appear as separate negative entries

- Bankruptcy: Chapter 7 stays for 10 years; Chapter 13 stays for 7 years

- Hard inquiries from multiple applications: Applying for several credit products in a short window stacks up inquiries fast

Late payments, high utilization, and bankruptcies can all affect your score for years, and your rights to dispute incorrect data are protected under the Fair Credit Reporting Act (FCRA). That is the federal law requiring bureaus to investigate disputes within 30 days.

Errors are more common than most people realize. Creditors sometimes report payments to the wrong account, or an old collection reappears after being removed. Reading your reports carefully at least once a year helps you catch these mistakes before a lender does.

“Negative items on your credit report do not just hurt your score. They signal risk to every lender, landlord, or business partner who checks your file.”

If you spot something wrong, you have the right to dispute it directly with the bureau holding the error. Understanding dealing with negative marks on your file gives you a clear starting point. Walking through the credit report dispute process step by step makes it far less overwhelming.

Pro Tip: Set recurring calendar reminders for every due date, not just your biggest bills. Subscription services, store cards, and medical payment plans are easy to forget and can quietly damage your score.

The special role of credit agencies for small business owners

The story is a bit different if you run a small business, where both personal and business credit matter more than most new owners expect.

When you first launch a business, lenders look straight at your personal credit score because your company has no financial track record yet. Small business owners need a strong personal score first, then build a business credit profile using tools like a DUNS number and vendors that report payment history to business bureaus.

Here is a step-by-step path to building real business credit:

- Separate your finances immediately. Open a dedicated business checking account and get a business credit card. Mixing personal and business spending makes it harder to build a distinct business profile.

- Register for a DUNS number. Dun and Bradstreet’s DUNS number is the standard business identifier used by lenders and suppliers. It is free and takes a few days to set up.

- Work with vendors that report to business bureaus. Office supply stores, fuel card companies, and certain wholesale suppliers report your payment history to Dun and Bradstreet, Experian Business, or Equifax Business. These trade lines build your business credit score.

- Pay vendors early when possible. Business credit scoring (like the Paydex score from Dun and Bradstreet) rewards early payments more than personal scoring models do.

- Monitor your business credit regularly. Business credit reports are not free the way personal reports are, but checking them quarterly helps you catch errors before they affect financing.

Common mistakes small business owners make include using personal cards for business purchases, skipping registration with business bureaus, and assuming that a healthy business bank account is enough to qualify for a small business loan.

The small business credit checklist at Credit Rebooter walks you through exactly what to set up so you can transition from relying on personal guarantees to building a truly independent business credit profile.

- Equifax Business, Experian Business, and Dun and Bradstreet are the main agencies tracking business credit

- The Paydex score (Dun and Bradstreet) runs from 1 to 100, unlike the 300 to 850 personal scale

- Business credit files are visible to the public, meaning your competitors and suppliers can check them

Why viewing credit agencies as ‘the enemy’ misses the mark

Most people treat credit bureaus like a mysterious force that controls their financial fate. We get it. When a score drops after one error or a missed payment you did not even know about, it feels like the system is rigged against you.

But here is the reality we have seen time and again: the people who improve their credit fastest are the ones who treat credit agencies as tools rather than opponents. Pulling your free reports is not admitting defeat. It is gathering intelligence. Disputing an error is not a confrontation. It is exercising a federal right that exists specifically to protect you.

Proactive monitoring your credit report can catch identity theft months before a fraudulent account ruins your score. Reviewing your reports before applying for a mortgage gives you time to fix mistakes that could cost you thousands in higher interest rates. Most people skip these steps and only look at their credit when it is already too late.

The bureaus are not perfect, and they are not your friends. But they are not working against you either. They are data systems, and like any system, knowing how they work gives you the upper hand.

Take the next step to improve your credit

You now have a clear picture of how credit agencies collect data, calculate scores, and affect both personal and business finances. Knowledge is only the first move. The real results come when you act on it.

At Credit Rebooter, we offer practical credit building strategies tailored to where you are right now, whether you are starting from scratch or trying to recover from past setbacks. If your score needs more than a tune-up, our credit score repair solutions can help you map a clear path forward. Not sure where to begin? Learn when to seek professional credit repair so you know exactly when it makes sense to bring in expert support.

Frequently asked questions

Why are my credit scores different at each agency?

Each bureau may hold different account data because not all lenders report to all bureaus, and each uses its own proprietary scoring model to calculate your number.

How long do negative items stay on my credit report?

Most negative items, including late payments, stay for seven years, while Chapter 7 bankruptcy stays on your report for up to 10 years under FCRA guidelines.

Can I dispute errors on all my credit reports?

Yes. Federal law requires each bureau to investigate disputes within 30 days of receiving your complaint, and they must correct or remove verified inaccuracies.

How do small business credit bureaus differ from personal credit agencies?

Business bureaus track company payment histories and trade lines rather than individual accounts, but most new business owners must maintain a strong personal score first before a business profile carries any real weight with lenders.