Credit monitoring sounds like it should fix your credit score automatically. Many people sign up expecting their numbers to climb, then feel let down when nothing changes. The truth is that credit monitoring is a tracking tool, not a repair tool. It watches your credit report for changes and alerts you when something happens, but it never disputes errors or removes negative items on your own behalf. This guide breaks down exactly what credit monitoring does, how free and paid options compare, and how you can use it as a real part of your DIY credit repair plan.

Table of Contents

- Understanding credit monitoring: What it is (and isn’t)

- Types of credit monitoring: Free vs. paid options

- How credit monitoring supports DIY credit repair

- Coverage gaps, limitations, and how to maximize protection

- What most people get wrong about credit monitoring

- Ready to take control? Credit Rebooter makes it easy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Monitors, not repairs | Credit monitoring tracks changes but does not fix credit errors automatically. |

| Free options are strong | DIYers can cover most needs with free tools like AnnualCreditReport.com and Credit Karma. |

| Act on alerts | The key to successful credit repair is acting on monitoring alerts and verifying results yourself. |

| Pair protection methods | For best safety, use credit monitoring with credit freezes and manual checks to defend your score. |

Understanding credit monitoring: What it is (and isn’t)

Credit monitoring is a service that watches your credit report and notifies you when something changes. Think of it like a security camera for your credit file. It records what happens, but it does not stop anything on its own.

Here is what credit monitoring actually does for you:

- Sends alerts when a new account is opened in your name

- Flags hard inquiries from lenders or creditors

- Notifies you of changes to your balances or payment status

- Warns you about potential signs of identity theft

- Shows score changes over time so you can track progress

Here is what credit monitoring does not do:

- File disputes with credit bureaus on your behalf

- Remove errors or negative items from your report

- Prevent fraud from occurring in the first place

- Guarantee your score will improve

For anyone working on DIY credit repair, this distinction is critical. Monitoring is your early warning system. It tells you when something needs your attention, but you are the one who has to act. As the FTC makes clear, credit monitoring does not file disputes or repair credit itself, meaning users must act on every alert they receive.

“Credit monitoring does not repair credit. Users must still act on alerts to see real results.”

Understanding credit repair laws helps you know your rights when you do decide to act. The Fair Credit Reporting Act gives you the power to dispute inaccuracies directly, but monitoring is simply the tool that helps you spot them first.

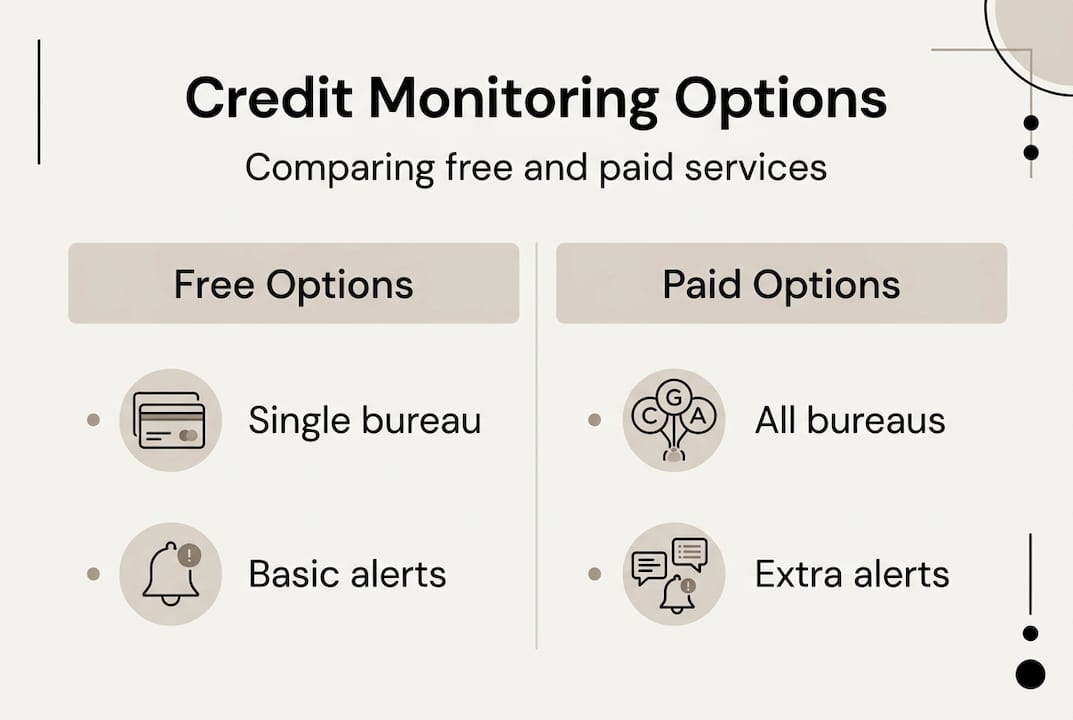

Types of credit monitoring: Free vs. paid options

Before you spend money on a monitoring service, it helps to know what is already available to you at no cost. Free options include AnnualCreditReport.com, Experian free monitoring, and Credit Karma, while paid services can run up to $30 per month or around $350 per year.

Free monitoring sources worth knowing:

- AnnualCreditReport.com: Federally mandated free weekly reports from all three bureaus

- Credit Karma: Free VantageScore updates from TransUnion and Equifax

- WalletHub: Daily credit score updates and report monitoring

- Bank and credit card portals: Many now offer free FICO score tracking built in

- Experian free tier: Monitors your Experian report and sends alerts

Paid plans typically run between $10 and $30 per month and often include three-bureau coverage, dark web scanning, identity theft insurance, and social security number monitoring. Family plans can reach $300 to $600 per year for broader household protection.

| Feature | Free options | Paid options |

|---|---|---|

| Bureau coverage | 1 to 2 bureaus | All 3 bureaus |

| Alert speed | Daily to weekly | Real-time |

| Dark web scanning | Rarely included | Usually included |

| Identity theft insurance | No | Often yes |

| Score model used | VantageScore | VantageScore or FICO |

| Monthly cost | $0 | $10 to $30 |

Data breaches have surged dramatically in recent years, making monitoring more relevant than ever. That growing risk is exactly why pairing monitoring with the steps to credit repair matters so much. Knowing your report changed is only useful if you know what to do next.

How credit monitoring supports DIY credit repair

Credit monitoring becomes genuinely powerful when you use it as part of a structured repair plan rather than as a standalone product. The key insight is this: monitoring tells you what happened, and your response determines what happens next.

Here is how a real DIY process looks when monitoring is built in:

- Pull your credit reports and identify errors, outdated accounts, or suspicious items

- File disputes directly with the relevant bureau for any inaccurate information

- Set up monitoring alerts so you are notified the moment the bureau updates your file

- Review the outcome once the dispute window closes, typically 30 to 45 days

- Repeat the process for any remaining issues, tracking score changes along the way

- Monitor new activity to make sure no new errors or fraud appear while you work

As the FTC confirms, credit monitoring verifies dispute outcomes and tracks score improvement, but it does not file disputes itself. That part is always on you.

Pro Tip: Combine credit monitoring with a credit freeze at all three bureaus. A freeze stops new accounts from being opened in your name, while monitoring catches anything that slips through. Together they give you far more control than either one alone.

For a deeper look at how this fits into a full strategy, the step-by-step credit repair process at Credit Rebooter walks you through each phase. And if you are focused on growth rather than just repair, building credit repair strategies can help you add positive history while you clean up the old stuff.

Coverage gaps, limitations, and how to maximize protection

No monitoring service covers everything. Knowing the gaps helps you build a smarter system around them.

The biggest limitations to watch for:

- Single-bureau gaps: If your service only monitors one bureau, you can miss major updates at the other two. Lenders report to different bureaus, and a serious delinquency might only show up on one report for weeks.

- Score model mismatches: Most free services use VantageScore. Most lenders use FICO. Your monitored score and your actual lender score can differ by 20 to 50 points, which means an alert may not reflect what a bank actually sees.

- Reactive, not proactive: Monitoring finds suspicious activity after it appears. It does not stop fraud before it happens.

- Alert fatigue: Too many notifications can cause you to start ignoring them, which defeats the purpose entirely.

| Limitation | How to address it |

|---|---|

| Single-bureau coverage | Use free reports from all three bureaus regularly |

| VantageScore vs. FICO gap | Check your FICO score through your bank or credit card portal |

| Reactive detection | Pair monitoring with a credit freeze at Equifax, Experian, TransUnion |

| Alert fatigue | Customize alert thresholds and review weekly, not daily |

| Dark web exposure | Add dark web scanning through paid tier or identity protection service |

Research from the Philadelphia Fed shows that fraud victims who use credit alerts can see a 12-point credit score increase, and 11% become prime borrowers after intervention. That is a meaningful outcome, but only for people who actually act on the alerts they receive.

The FTC recommends pairing monitoring with a credit freeze for best results, since monitoring detects but does not prevent fraud. Understanding your rights under credit reporting laws gives you the legal tools to act fast when something goes wrong. And if you ever receive an alert that looks suspicious, the guidance at credit monitoring warnings can help you figure out your next move.

Pro Tip: Set a calendar reminder every two weeks to manually log in and review your reports, even if you have not received any alerts. Automated systems miss things, and your own eyes are still your best defense.

What most people get wrong about credit monitoring

Here is the uncomfortable truth that most guides skip over: credit monitoring is one of the most misunderstood products in personal finance. People buy it expecting results and get information instead. That gap between expectation and reality is where frustration lives.

The FTC is clear that free DIY monitoring through free reports is sufficient for vigilant consumers, and that monitoring is not a repair tool. Yet the industry markets these services as if they will do the heavy lifting for you.

The consumers who actually improve their credit do something different. They treat monitoring as a feedback loop, not a solution. They check alerts, investigate every flag, file disputes when needed, freeze their credit proactively, and review their reports manually on a schedule. They use do-it-yourself credit repair tips to stay ahead of problems rather than waiting for a service to fix things automatically.

The real secret is that your action is the only ingredient that actually moves your score. Monitoring just makes sure you have the information to act on. Treat it like a dashboard, not a driver.

Ready to take control? Credit Rebooter makes it easy

Now that you understand how credit monitoring fits into a real repair strategy, the next step is putting that knowledge to work. Credit Rebooter gives you the tools and guidance to move from awareness to action.

Whether you are just starting to explore credit-building strategies or you are ready to tackle existing damage head-on with credit score repair, Credit Rebooter has resources built specifically for people like you. Our learning center, free tools, and expert support are designed to turn what you have learned here into real, measurable progress on your credit report. You have the knowledge. Now let’s put it to work.

Frequently asked questions

Does credit monitoring help improve your credit score?

Credit monitoring itself does not raise your score, but it helps you catch problems early and act quickly, which protects and supports improvement over time. The repair happens when you respond to what monitoring reveals, not from the monitoring itself.

Is it safe to use free credit monitoring services?

Free services are generally safe when you stick to reputable providers. Free options like AnnualCreditReport.com, Experian, and Credit Karma are well-established and widely trusted by consumers.

What is the difference between credit monitoring and a credit freeze?

Credit monitoring alerts you when changes appear on your report, while a credit freeze actively blocks new accounts from being opened in your name. Pairing both gives you the strongest protection available.

Should I pay for three-bureau monitoring?

Three-bureau coverage gives you the most complete picture, but free options work well if you use them consistently and proactively. Single-bureau gaps are real, so supplement free services with manual checks across all three bureaus.