Starting your financial life with no credit history is like showing up to a job interview with a blank resume. Lenders can’t see who you are, so they assume the worst, or simply turn you away. Millions of Americans face this exact situation every year, whether they’re recent graduates, new immigrants, or adults who’ve simply avoided credit. The good news is that building credit from zero is completely doable, and it doesn’t require tricks or luck. This guide walks you through the fundamentals, the best tools, the right habits, and the mistakes to avoid so you can build a solid credit profile step by step.

Table of Contents

- Understanding credit basics and why it matters

- Get started: Practical ways to build credit from zero

- Step-by-step: Open and manage your first credit account

- Mistakes to avoid and troubleshooting your credit journey

- How to track your progress and reach your first score

- What most guides get wrong about building credit from scratch

- Take the next step with trusted credit building solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Credit building is a process | Building credit from scratch takes time and steady habits, not quick fixes. |

| Use multiple starter tools | Combining secured cards and credit-builder loans sets a solid foundation and improves your credit mix. |

| Avoid costly mistakes | Pay on time, keep balances low, and avoid products that don’t report activity. |

| Track your score progress | Monitor your credit report and set realistic goals to stay motivated. |

Understanding credit basics and why it matters

With the problem of no credit in mind, let’s start by understanding the fundamentals of what credit is and why it matters.

Credit is essentially your track record of borrowing money and paying it back. Lenders, landlords, and even some employers use your credit score to decide whether to trust you with money, a lease, or a job. The most widely used score is the FICO score, which ranges from 300 to 850. The higher the number, the better you look to lenders.

Your FICO score is calculated using five key factors, and knowing them helps you focus on what actually moves the needle:

| FICO factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | On-time vs. late payments |

| Amounts owed (utilization) | 30% | How much of your available credit you use |

| Length of credit history | 15% | Age of your oldest and newest accounts |

| New credit | 10% | Recent applications and hard inquiries |

| Credit mix | 10% | Variety of credit types (cards, loans, etc.) |

As you can see, FICO score factors like payment history and utilization together make up 65% of your score. For beginners, that means two things matter most: pay on time, every time, and keep your balances low relative to your credit limit.

Here’s something that surprises most first-timers: having no credit is not the same as having bad credit. Bad credit means you have a history of missed payments or defaults. No credit means there’s simply nothing to evaluate. Both situations make borrowing harder, but they require different solutions. You can learn more about building credit history and why the distinction matters when you’re choosing your first steps.

A score of 670 or higher is generally considered “good” by most lenders, and reaching that milestone opens doors to better interest rates, higher credit limits, and more financial options.

To get your first FICO score, you need at least one account that has been open for six months with recent activity. That’s your starting line. From there, responsible behavior compounds over time.

Get started: Practical ways to build credit from zero

Now that you know why credit matters, let’s focus on the most actionable tools to start your credit journey.

There are several proven methods to build credit when you’re starting from nothing. The primary methods to build credit from scratch include secured credit cards, credit-builder loans, becoming an authorized user on someone else’s account, rent and utility reporting services like Experian Boost, and student or retail credit cards. Each has its own strengths depending on your situation.

Here’s a quick comparison to help you choose:

| Method | Best for | Key benefit | Main risk |

|---|---|---|---|

| Secured credit card | Most beginners | Fast utilization reporting | Overspending temptation |

| Credit-builder loan | Disciplined savers | Builds installment history | Monthly payment commitment |

| Authorized user | Those with trusted family/friends | Instant history boost | Inherits primary user’s negatives |

| Rent/utility reporting | Renters already paying bills | No new account needed | Limited bureau coverage |

| Student/retail card | College students | Easy approval | High interest rates |

What you’ll generally need to qualify for each option:

- Secured card: A refundable deposit (usually $200 or more), a bank account, and a valid ID

- Credit-builder loan: Proof of income or employment, offered through credit unions and community banks

- Authorized user: A family member or close friend willing to add you to their account

- Rent reporting service: A history of on-time rent payments and a compatible landlord or service

When it comes to secured cards vs credit-builder loans, both serve different purposes. Cards help you build revolving credit and demonstrate utilization management faster. Loans build installment credit history with a built-in savings component. Using both together can actually improve your credit mix, which accounts for 10% of your FICO score.

Pro Tip: Don’t try to open five accounts at once. Start with one secured card and one credit-builder loan, use them responsibly for six months, and then reassess. Slow and steady wins here.

You can explore more credit building strategies to find the combination that fits your income and lifestyle.

Step-by-step: Open and manage your first credit account

With your tools picked out, here’s exactly how to open and handle your new credit-building account without damaging your score.

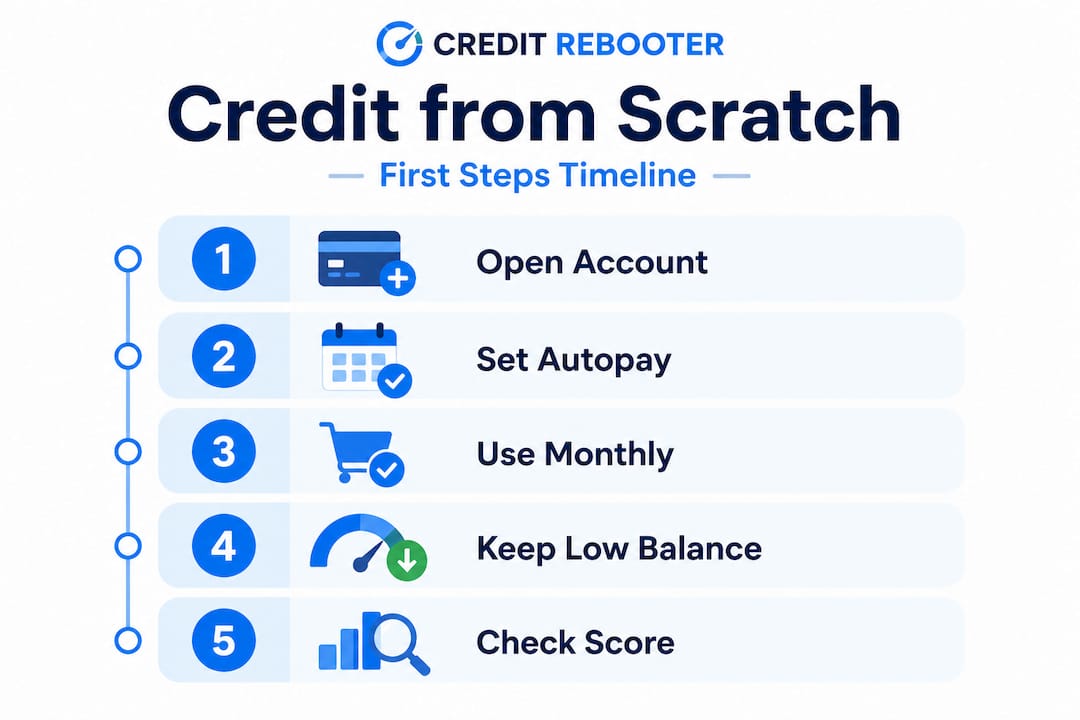

Opening a secured credit card is the most common first step, and it’s simpler than most people expect. Here’s how to do it right:

- Choose a card that reports to all three bureaus. Not all secured cards report to Experian, Equifax, and TransUnion. Make sure yours does, or your effort won’t build a score.

- Make your deposit. Secured credit cards require a refundable deposit between $100 and $1,000, which becomes your credit limit. Start with $200 to $300 if possible.

- Activate the card and set up autopay. Autopay for the minimum payment protects you from accidental late payments. Then manually pay the full balance before the due date each month.

- Make one or two small purchases per month. Think gas, groceries, or a streaming subscription. Keep the total under 10% of your credit limit.

- Pay the full balance monthly. Carrying a balance does not help your score and costs you interest. Pay it off completely every month.

- Check for an upgrade offer after 6 to 12 months. Many issuers will convert your secured card to an unsecured card and return your deposit once you’ve shown responsible behavior.

If you prefer a credit-builder loan, the process is slightly different. Credit-builder loans hold the loan amount (typically $300 to $1,000) in a savings account while you make fixed monthly payments over 6 to 24 months. At the end, you get the money back. It’s essentially a forced savings plan that also builds your credit. The risk of overspending is zero because you never touch the money until the loan is paid off.

Here’s a real-world example: Imagine you open a secured card with a $300 deposit and charge $25 per month for groceries. That’s a utilization rate of about 8%. You pay it in full each month. After six months, you have a FICO score. After twelve months, you’re likely approaching the 670 “good” range. Simple, boring, and it works.

Statistic to know: Keeping utilization between 1% and 9% is associated with an average FICO score of 753, while utilization between 30% and 49% drops that average to 685. A single missed payment can lower your score by 60 to 110 points. The math is clear.

Pro Tip: Set a calendar reminder three days before your payment due date. Even with autopay, a manual check prevents surprises from bank delays or billing errors.

To avoid common mistakes that could set you back, read more about how to build your credit with caution.

Mistakes to avoid and troubleshooting your credit journey

Once your new account is active, it’s easy to slip up if you’re not careful. Here’s what to avoid and how to stay on track.

Common rookie mistakes that hurt first-time credit builders:

- Over-utilizing your credit limit. Charging more than 30% of your limit in a billing cycle, even if you pay it off, can temporarily spike your utilization score.

- Making a late payment. Even one missed payment can drop your score dramatically and stays on your report for seven years.

- Relying solely on authorized user status. This is a passive strategy. It helps, but it doesn’t replace building your own accounts.

- Not checking your credit reports. Errors on your report are more common than you’d think, and they can silently drag your score down.

- Applying for too many accounts at once. Each application triggers a hard inquiry, which can lower your score by a few points and signals desperation to lenders.

Warning: Some products are marketed as credit-building tools but do nothing for your score. Prepaid debit cards and payday loans are two of the biggest examples. They don’t report to credit bureaus, and payday loans can trap you in a debt cycle that damages your finances without ever helping your credit.

You should check free weekly reports at annualcreditreport.com and dispute any errors you find. The dispute process is free and can result in score improvements within 30 to 45 days if the error is removed.

If something does go wrong, here’s how to troubleshoot:

- Missed a payment? Pay it immediately. The damage is done, but catching up fast limits the long-term impact. Set up autopay going forward.

- Application denied? Ask for the denial letter, which must explain why. Use that information to address the specific issue before applying again.

- Score dropped unexpectedly? Check your report for new errors, a sudden increase in utilization, or an account that was closed.

It also helps to know which options to avoid in credit repair so you don’t waste time or money on products that sound helpful but aren’t.

How to track your progress and reach your first score

To stay motivated and avoid guessing, it’s crucial to track your improvement the right way.

Here’s what healthy credit progress looks like over your first year:

| Timeline | Milestone | What to focus on |

|---|---|---|

| Month 1 to 3 | Account open, no score yet | Set up autopay, make small purchases |

| Month 4 to 6 | First FICO score appears | Confirm utilization is under 10% |

| Month 7 to 9 | Score in the 580 to 640 range | Add a second account if ready |

| Month 10 to 12 | Score approaching 670+ | Review report, dispute any errors |

Your first FICO score requires at least one account open for six months with recent activity. A good score of 670 or higher typically takes 12 to 18 months of responsible behavior. Secured cards tend to give you a faster initial boost because utilization is reported monthly, while credit-builder loans contribute steady installment history over time.

Activities that accelerate your progress:

- Paying every bill on time, including utilities if you use a reporting service

- Keeping utilization consistently below 10%

- Avoiding unnecessary hard inquiries

- Letting accounts age without closing them

- Adding a second credit type (card plus loan) after six months

The empirical benchmarks are clear: utilization at 1% to 9% averages a 753 FICO score, while jumping to 30% to 49% drops that average by 68 points. A late payment hurts between 60 and 110 points. A diverse mix combined with low utilization can push you past 700 within 12 to 24 months.

To monitor your score without hurting it, use free tools offered by your card issuer or apps like Credit Karma. These use “soft” inquiries that don’t affect your score. Avoid applying for new credit just to check your options. For more detailed guidance, check out these tips on how to improve your credit score as your profile grows.

What most guides get wrong about building credit from scratch

Before you finalize your credit journey plans, it’s worth hearing the truth most articles skip.

Most beginner guides hand you a list of tools and send you on your way. What they rarely say is that the biggest threat to your credit-building success isn’t a lack of knowledge. It’s impatience fueled by bad advice found on social media.

Credit “hacks” circulate constantly on platforms like TikTok and Instagram. You’ve probably seen them: “Add yourself as an authorized user on five cards,” “Apply for a business card to bypass personal credit checks,” “Use this trick to get a $10,000 limit in 30 days.” These tactics aren’t just risky. They’re often slower than simply doing things the right way. When you chase shortcuts, you spend energy gaming a system that rewards consistency. And when the hack backfires, such as a hard inquiry you didn’t expect or a primary user who misses payments, you’re worse off than when you started.

We’ve seen this pattern repeatedly. Someone spends three months trying to optimize every angle, applying for cards they don’t qualify for, chasing authorized user spots on strangers’ accounts through online forums, and obsessing over every point fluctuation. Meanwhile, someone else opens one secured card, charges their Netflix subscription, pays it off monthly, and quietly crosses the 670 mark without stress.

The boring approach wins. Not because it’s clever, but because credit scoring rewards exactly one thing over time: predictable, responsible behavior. You can explore easy tricks to use for credit repair that are actually legitimate, but the foundation is always the same: pay on time, keep balances low, and let time do its work.

A balanced approach, using both a secured card and a credit-builder loan, builds a healthier profile than stacking five credit cards. It demonstrates to lenders that you can manage different types of credit, which is exactly what the credit mix factor rewards. Trust the process. Discipline is the only real shortcut.

Take the next step with trusted credit building solutions

If you’re ready to take your next confident steps, here’s where to go for more help and support.

Building credit from scratch takes time, but you don’t have to figure it all out alone. Whether you’re just opening your first secured card or you’re several months in and want to accelerate your progress, having the right guidance makes a real difference.

At Credit Rebooter, we’ve built a full library of resources designed specifically for people in your position. From detailed guides on improving your credit score to personalized credit assistance through our online registration, we’re here to help you move from invisible to financially confident. Our learning center covers everything from credit score fundamentals to debt elimination strategies, and it’s free to explore. If your situation is more complex, our team can walk you through a customized plan. Take the next step today and let us help you build the credit profile you deserve.

Frequently asked questions

How long does it take to establish a credit score from scratch?

It usually takes at least 6 months after opening your first account with activity to get your initial FICO score, as one account open 6+ months with recent activity is the minimum requirement.

What’s the fastest way to start building credit with no history?

Opening a secured credit card and making small purchases paid off each month is the fastest route, since secured cards report to all bureaus and can show an upgrade path to unsecured credit in as little as 6 to 12 months.

Can I build credit if I’m not a U.S. citizen or don’t have a Social Security number?

Yes, some secured cards accept ITINs or foreign passports, since some secured cards accept ITIN/passport for non-citizens, though prior foreign credit history does not transfer to U.S. bureaus.

Do prepaid or debit cards help build credit?

No. Prepaid and debit cards do not report to credit bureaus, so using them does nothing to establish or improve your credit history.

Should I become an authorized user on someone else’s card?

It can help if the primary account has a long, clean history and low utilization, but authorized user negatives transfer too, making it smarter to build your own accounts as the primary strategy.