Two buyers purchase identical homes for $350,000. One has a 760 credit score; the other has a 640. Over 30 years, the second buyer pays tens of thousands more in interest — for the exact same house. That’s not a hypothetical. Improving your score to 760 can save between $20,000 and $46,000 in interest over the life of a loan, depending on your state and home price. Your credit score isn’t just a number lenders glance at — it’s a pricing engine that determines your rate, your monthly payment, and how much of your wealth quietly drains away over the next three decades.

Table of Contents

- Understanding credit’s influence on home buying

- Minimum credit scores for common loan types

- How your credit affects mortgage rates and costs

- Boosting your credit before applying: what works and what to avoid

- Why buyers often misunderstand credit’s role — and what really moves the needle

- Get expert help to strengthen your credit for home buying

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Credit is crucial | Your credit score is the most important factor in qualifying for a mortgage and getting the lowest rates. |

| Loan options vary by score | Different home loans have different minimum score requirements and lender rules. |

| Better credit saves money | Higher scores can save you tens of thousands of dollars over the loan’s lifetime. |

| Holistic underwriting matters | Lenders look at not just your score, but also debts, income, and assets. |

| Lasting improvement takes time | With patience and smart moves, most buyers can achieve meaningful credit gains before they buy. |

Understanding credit’s influence on home buying

Most buyers assume lenders just check your score, see if it clears a threshold, and either say yes or no. The real picture is more layered than that, and understanding it gives you a major edge.

Mortgage underwriters don’t evaluate credit in isolation. They use a framework often called the “4 Cs” of underwriting to assess your full financial profile. These are:

- Credit: Your FICO score, payment history, types of accounts, and any derogatory marks

- Capacity: Your ability to repay, primarily measured by your debt-to-income (DTI) ratio

- Capital: Your savings, reserves, and down payment

- Collateral: The appraised value and type of property you’re buying

Your credit score dominates one of those four pillars, but lenders are evaluating all of them together. For example, conventional loans max DTI at 45-50%, while FHA loans allow up to 43-50% depending on compensating factors. A buyer with a 700 score and a 30% DTI looks much stronger than one with a 740 score and a 55% DTI. Credit and capacity interact constantly.

“Your credit score is the most important factor in determining your interest rate, but lenders are underwriting your entire financial life — not just a single number.”

This matters because it means improving your credit score is only part of your preparation. You also need stable income, manageable debt, and enough reserves to show lenders you’re not one unexpected car repair away from missing a payment.

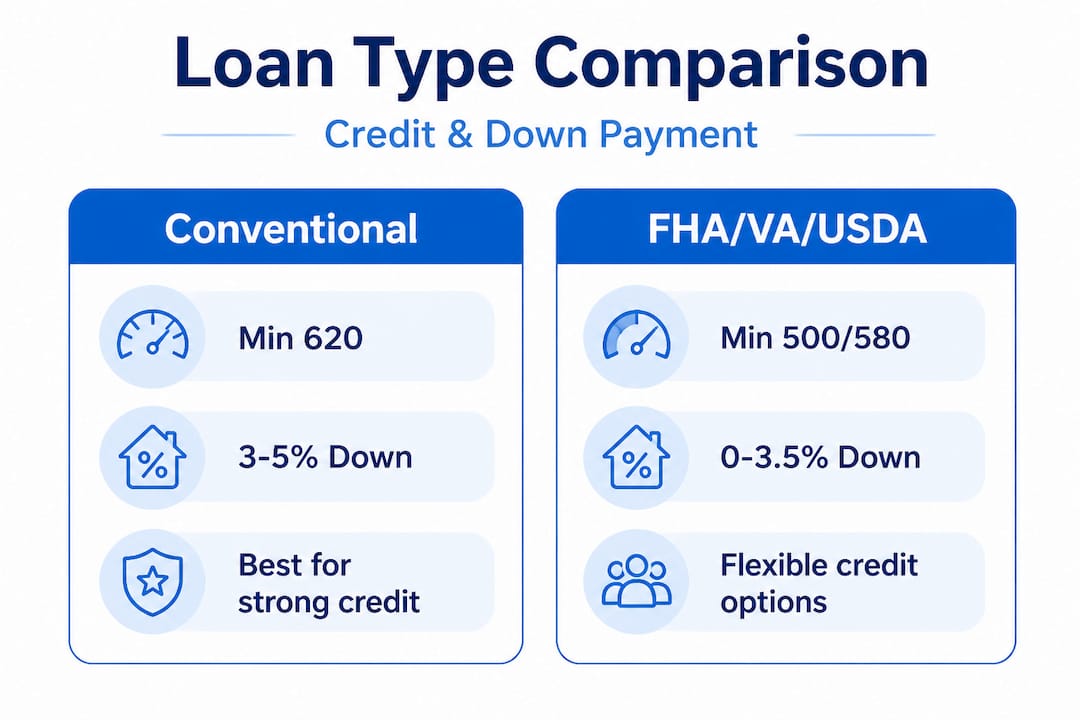

Minimum credit scores for common loan types

Once you understand that credit is one component of a larger evaluation, you’ll want to know where you actually stand relative to each loan program’s requirements.

Here’s a straightforward comparison of the four most common mortgage types and their minimum credit score thresholds:

| Loan type | Minimum FICO score | Down payment minimum | Notes |

|---|---|---|---|

| Conventional | 620 | 3-5% | Lender overlays common; better rates at 740+ |

| FHA | 580 (500 with 10% down) | 3.5% (or 10%) | More lenient on credit history |

| VA | No official minimum | 0% | Most lenders overlay 580-640 |

| USDA | No official minimum | 0% | Most lenders overlay 580-640; rural areas only |

According to updated credit score mortgage guidelines, Fannie Mae recently removed a hard minimum for its Desktop Underwriter automated system, emphasizing a more holistic review. That doesn’t mean low scores sail through — it means strong compensating factors can sometimes override a borderline number.

A few things worth knowing about how lenders apply these thresholds:

- Lender overlays are real. Even if a program technically allows a 580 score, many lenders set their own minimum at 620 or even 640. Always ask about the lender’s internal requirements.

- Manual underwriting creates flexibility. If automated systems decline you, some lenders offer manual underwriting, where a human reviewer weighs your full profile. Strong reserves and a clean recent payment history help here.

- Co-signers and larger down payments can compensate. A co-signer with better credit or a down payment above 20% can offset a below-average score in specific situations.

- Recent negative items hurt more than old ones. A missed payment from five years ago matters far less than one from six months ago.

Pro Tip: Before applying for a mortgage, pull all three of your credit reports from Annualcreditreport.com and review them carefully. Errors are more common than most people expect, and disputing them before you apply is one of the fastest ways to get a score boost with no extra effort required. You can also visit credit score tips for homebuyers for a clear action plan.

How your credit affects mortgage rates and costs

Knowing you qualify is one thing. Knowing exactly how much a higher score would save you is where things get really motivating.

Lenders use something called Loan-Level Price Adjustments (LLPAs) to price mortgage rates. These are fees added to the cost of a conventional loan based on your FICO score and your loan-to-value (LTV) ratio. The lower your score and the more you borrow relative to the home’s value, the more you pay.

Here’s what the LLPA matrix looks like in practice for an 80-85% LTV loan:

| FICO score range | Approximate LLPA fee |

|---|---|

| 780 and above | 0% to 0.25% |

| 740-779 | 0.25% to 0.5% |

| 720-739 | 0.5% to 0.75% |

| 700-719 | 0.75% to 1.0% |

| 680-699 | 1.0% to 1.5% |

| 660-679 | 1.5% to 2.0% |

| 640-659 | 2.0% to 2.5% |

| Below 640 | Up to 2.875% |

These percentage points add up fast. On a $350,000 loan, a 2.875% LLPA is nearly $10,000 added to your loan cost upfront — or folded into a higher interest rate you pay for 30 years.

The CFPB’s rate exploration tool shows that on a $400,000 home, the difference between a 625 and a 700 FICO score can translate to up to $264,000 in lifetime interest costs. That’s not a rounding error. That’s a college education, a rental property, or years of retirement income.

Key takeaways on how scores shape your rate:

- Scores below 640 trigger the steepest fees and the highest rates

- Moving from the 660 range to 700 is often worth more financially than moving from 740 to 780

- The biggest rate improvement typically comes between the 620 and 760 range

- Above 760, there are diminishing returns — the incremental savings per additional point shrink significantly

Pro Tip: If your score sits at 698 or 718, pushing it just a few points into the next band (700 or 720) can meaningfully drop your LLPA fee. Sometimes paying down a single credit card balance before application day is all it takes. Review steps to raise your credit score to find the fastest legitimate moves available to you.

Boosting your credit before applying: what works and what to avoid

If you’re 12 to 36 months away from applying for a mortgage, you have a real opportunity to change your rate tier entirely. The realistic improvement pace is about 20 points per year, which means getting from an average score around 700 to the 760 threshold takes roughly 1.5 to 3 years of consistent effort.

Here are the highest-impact steps to take before you apply:

- Pay every bill on time, without exception. Payment history makes up 35% of your FICO score. A single 30-day late payment can drop your score by 50 to 100 points, and it stays on your report for seven years.

- Lower your credit utilization below 30%, ideally below 10%. Utilization is the second biggest factor. If you carry $4,000 on a card with a $5,000 limit, you’re at 80% utilization. Paying that down to $500 can move your score by 30 to 50 points relatively quickly.

- Dispute errors on your credit reports. Incorrect late payments, duplicate accounts, or fraudulent accounts can drag your score down unfairly. Disputing them before application is one of the cleanest wins available.

- Avoid opening new accounts before applying. New credit inquiries and new account age can temporarily lower your score. The six months before your mortgage application is not the time to open a new store card.

- Don’t close old credit card accounts. Closing accounts reduces your available credit and shortens your average account age, both of which can hurt your score.

Equally important is knowing what to avoid:

- Don’t pay off old collections right before application without advice. Paying a collection can sometimes re-age the account and temporarily lower your score, especially with older negative items.

- Don’t max out cards even temporarily. Even if you pay the full balance at the end of the month, if the statement closes while the balance is high, that high utilization still gets reported.

- Don’t co-sign new loans for others. That debt shows on your credit profile and increases your DTI.

Low scores in the 500-579 range aren’t necessarily disqualifying. FHA loans allow buyers in that range with a 10% down payment, and manual underwriting with compensating factors like strong reserves or a very low DTI can sometimes offset a marginal score. But the costs are real, and the rates are high. Starting work on improving your credit before buying gives you options that waiting simply doesn’t.

“The best time to start building your credit for a home purchase was two years ago. The second best time is right now.”

For buyers who want a structured path forward, credit building strategies can help you prioritize the right moves based on your specific credit profile and timeline.

Why buyers often misunderstand credit’s role — and what really moves the needle

Here’s something most articles won’t tell you directly: obsessing over your credit score number is not the same as building a strong mortgage application.

Many buyers spend months laser-focused on nudging their score from 748 to 762, believing that crossing the magical “760 threshold” will unlock dramatically better rates. And while that jump does matter, they’re often ignoring things that matter just as much: carrying a 52% DTI ratio, having only two months of reserves, or sitting on a job gap from 18 months ago that will require explanation letters.

Lenders are looking at a picture, not a scorecard. Higher credit generally earns better terms, but the nuances — like lender overlays and the interaction between score and DTI — often determine who actually gets approved at the best rate.

We’ve also seen buyers burn time on “rapid rescore” tactics and credit repair shortcuts that look impressive on paper but don’t hold up to underwriter scrutiny. A mortgage underwriter will ask for 12 to 24 months of statements. They will see that a credit card balance went from $8,000 to $200 in the month before application. That kind of sudden cleanup doesn’t fool anyone.

What actually moves the needle? Steady, consistent behavior over 12 to 24 months. No late payments. Gradually lower balances. No new accounts right before application. Those aren’t exciting tactics, but they’re the ones that translate directly into a lower rate on closing day.

Don’t waste energy chasing 800+. Above 760, the gains are minimal and the effort is disproportionate. Instead, focus on easy credit repair tips that eliminate red flags and build a clean, stable history that any lender will respond to favorably.

The buyers who get the best mortgage rates aren’t always the ones with the highest scores. They’re the ones who showed up with the most complete, consistent, and well-managed financial profile.

Get expert help to strengthen your credit for home buying

Knowing what to do and actually executing it are two very different things — especially when your financial future is on the line.

Credit Rebooter exists to help buyers like you close that gap. Whether you’re starting from scratch, recovering from past credit damage, or just trying to push your score into a better rate tier before applying, our credit score repair service gives you personalized guidance designed around your specific situation. We don’t offer generic advice — we look at your actual credit profile and build a plan that targets the factors holding your score back the most. You can also explore our improving your credit score resources and check your funding readiness to see exactly where you stand before you walk into a lender’s office.

Frequently asked questions

What is the minimum credit score for a conventional mortgage?

Conventional loans require a minimum 620 FICO, though most lenders set their own internal minimums higher, and better rates kick in significantly at 740 and above.

How much can a higher credit score really save when buying a home?

Up to $264,000 in lifetime savings is possible on a $400,000 home when comparing a 625 score to a 700 score, while boosting to 760 typically saves $20,000 to $46,000 over 30 years.

Can I get a loan with bad credit?

FHA loans allow scores as low as 500 with a 10% down payment, and manual underwriting with compensating factors like low DTI or strong reserves can sometimes help borderline applicants qualify.

How quickly can I improve my credit for a mortgage?

A realistic improvement pace is about 20 points per year, meaning most buyers reach major milestones like the 760 threshold in 1.5 to 3 years of steady, consistent effort.

Does a perfect score matter, or is there a point where higher scores don’t help more?

Benefits diminish above 760, so chasing 800+ rarely produces meaningful rate improvements — your energy is better spent maintaining a clean record and managing your full financial profile instead.