Most people assume credit repair means finding errors on their report and filing disputes until the bad stuff disappears. That worked as a partial strategy years ago, but 2026 has fundamentally changed the game. New scoring models reward sustained patterns over point-in-time fixes, which means a single successful dispute does far less for your score than building consistent, positive financial habits month after month. In this article, we’ll walk through the major trends reshaping credit repair, explain how new models like FICO 10T and VantageScore 4.0 actually evaluate you, highlight the pitfalls that trip up both individuals and small business owners, and give you the concrete strategies that are proven to work right now.

Table of Contents

- Key credit repair trends shaping 2026

- How new credit scoring models impact individuals and small businesses

- Common credit repair pitfalls to avoid in 2026

- Credit repair strategies that work in today’s environment

- What most credit repair advice misses in 2026

- Next steps: Get help with credit repair for 2026

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Behavior matters more | New scoring models reward ongoing good financial habits, not just disputes. |

| Watch for scams | Legal compliance and avoiding upfront payments are essential in 2026 credit repair. |

| Utilization impacts scores | Lowering your credit card balances consistently can help improve your score. |

| Businesses need tailored tactics | Small business owners should align credit repair efforts with lender requirements due to fast-changing criteria. |

Key credit repair trends shaping 2026

The credit repair landscape in 2026 looks very different from even three years ago. A few major forces are driving this change, and understanding them helps you make smarter decisions about where to put your energy.

AI-powered dispute workflows have become standard in the industry. These tools can scan credit reports, flag potential errors, and generate dispute letters faster than ever before. However, speed does not equal legality. The automation boom has also created room for shady operators who promise results they cannot legally deliver. FTC consumer guidance warns consumers to avoid scams that frame themselves as tech-powered solutions while still breaking federal rules.

What are those rules? Two big ones: credit repair organizations cannot legally charge you before services are fully performed, and no company can promise to remove accurate, up-to-date negative information from your report. It simply cannot be done, regardless of how sophisticated the software appears. Reviewing credit repair regulations before signing any service contract is one of the smartest moves you can make.

Trended data scoring is the other major shift. Models like FICO 10T and VantageScore 4.0 now evaluate your credit behavior over time rather than a snapshot of today’s numbers. Think of it like a report card versus a single quiz score. A lender using trended data can see whether your balances have been creeping up, holding steady, or consistently declining over the past 24 months. That longer view rewards responsible behavior and penalizes people who game the system with short-term tactics.

For a cleaner look at how approaches compare, here’s a quick breakdown:

| Approach | Old model thinking | 2026 model thinking |

|---|---|---|

| Dispute strategy | File disputes, wait for removal | Disputes fix errors only; behavior drives scores |

| Credit utilization | Keep it low at snapshot | Keep it consistently low month over month |

| Payment history | On-time payments help | Ongoing consistency is heavily weighted |

| Business credit | Separate from personal | Increasingly linked and trended |

| Fraud prevention | Occasionally checked | High-priority filter for lenders and bureaus |

For a broader view of what 2026 looks like across the industry, the 2026 credit repair overview on our site breaks it down further.

How new credit scoring models impact individuals and small businesses

With those industry shifts in mind, here is how these changes directly affect your score and what lenders actually see when they pull your credit.

FICO 10T uses up to 24 months of trended payment and balance data to evaluate creditworthiness. VantageScore 4.0 follows a similar logic, designed to reflect credit behavior over time rather than a single point in time. Both models reward people who show sustained positive patterns. That is a significant departure from older scoring systems that only cared about your current numbers.

What does this mean in practical terms? If you paid off a large credit card balance last month but had been carrying a high balance for the previous 18 months, your score bump will be smaller than you expect. The model sees the full picture and weighs the pattern, not just the most recent action. Conversely, if you have been steadily reducing your balances every single month for the past year, that trend signals financial discipline to lenders.

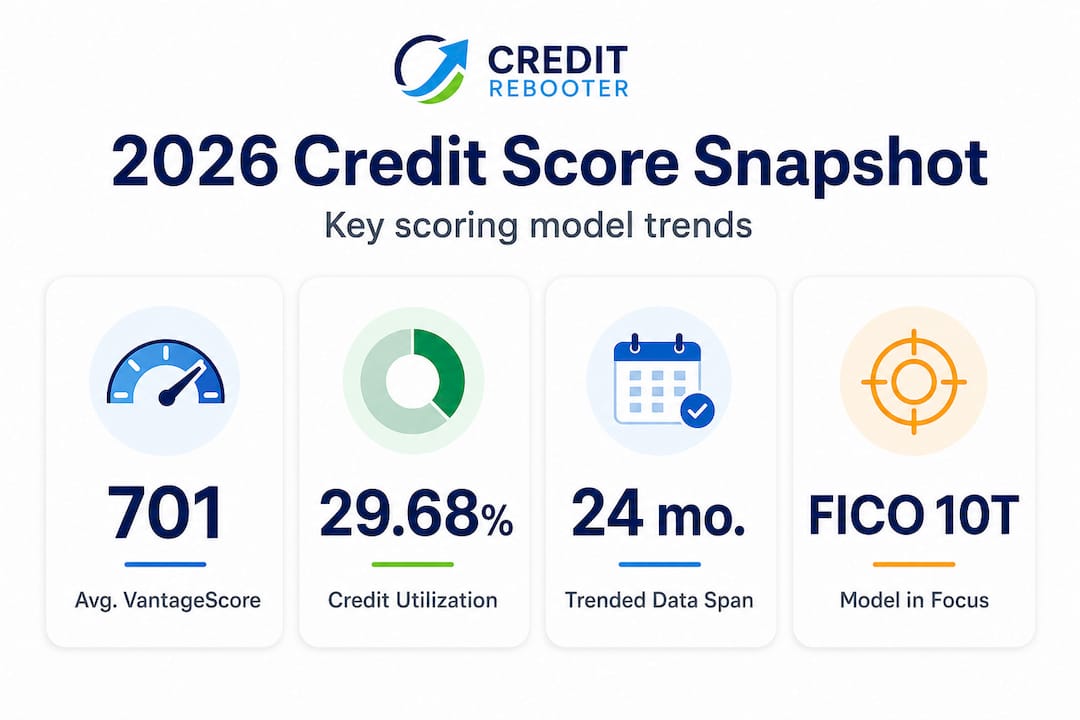

Here is what the data shows about where consumers stand right now:

| Metric | March 2026 figure |

|---|---|

| Average VantageScore 4.0 | 701 |

| Average credit utilization | 29.68% |

| Trend | Delinquencies declining |

The average VantageScore 4.0 held steady at 701 in March 2026, with utilization dropping to 29.68%. Consumers are pulling back on borrowing and paying down card balances, and the scoring models are rewarding exactly that behavior.

For small business owners, the implications run even deeper. Your lenders are increasingly looking at how your business credit profile evolves over time, not just whether you had a clean report at the time of application. If your business carries revolving balances that fluctuate wildly from month to month, that pattern raises flags. Steady, predictable credit usage gives lenders confidence that you manage cash flow responsibly.

Here are the key factors that matter most under the new models:

- Consistent on-time payments across all open accounts, every billing cycle

- Declining or stable revolving balances, especially month-over-month trends

- Low utilization ratio, ideally below 30% and trending downward

- Age of accounts, because older accounts with clean histories carry extra weight

- Mix of credit types, including installment loans and revolving accounts

Pro Tip: If you are carrying balances on multiple cards, focus on paying down the highest-utilization card first while making minimums on the others. This approach improves both your overall utilization ratio and the trended behavior your score tracks over time.

The building credit strategies page offers more specific guidance on structuring your accounts to maximize the benefit of trended data scoring.

Common credit repair pitfalls to avoid in 2026

Knowing how the new models work, let’s explore where repair efforts often go wrong, because these mistakes can actually make your situation worse rather than better.

-

Paying upfront for credit repair services. This is not just a bad deal, it is illegal. The Credit Repair Organizations Act (CROA) prohibits any company from charging you before they have fully performed the promised services. If a company asks for payment up front, walk away immediately.

-

Believing promises to remove accurate negative information. No legitimate company can remove accurate, current negative information from your credit report. FTC guidance is crystal clear on this point. Late payments, charge-offs, and collections that are accurately reported will stay until the reporting period expires, typically seven years.

-

Using synthetic identity or false fraud claims. Some disreputable services suggest filing false identity theft claims to remove legitimate negative accounts. Beyond being fraudulent, this approach is increasingly detectable. The credit bureaus and lenders have significantly upgraded their fraud detection systems in 2026, making this tactic far riskier than it was before.

-

Ignoring lender-specific underwriting criteria. Especially for small businesses, your credit score is just one piece of the picture. Lenders evaluate debt service coverage ratios, time in business, and cash flow statements. A small business owner who focuses entirely on personal credit scores while ignoring business financial documentation will be blindsided at the loan application stage.

-

Treating credit repair as a one-time project. Perhaps the biggest mistake of all. With trended data models in play, a single good month no longer carries the weight it once did. Credit repair in 2026 is an ongoing practice, not a one-time fix.

“The most effective credit repair strategy is not what happens during a dispute. It is what happens every single month for the next two years. Lenders are watching the pattern, not the moment.”

Reviewing the list of credit repair practices to avoid can help you recognize red flags before they cost you time and money. And if you have already experienced the consequences of bad advice, the risks with bad credit repair resource covers how to course-correct.

Credit repair strategies that work in today’s environment

Now, let’s break down the approaches that can actually move the needle for your credit in 2026 and beyond. These are not hacks or shortcuts. They are the habits that modern scoring models are specifically designed to reward.

The foundation remains the same as it always has been: pay on time and keep your balances low. But the way you do this matters more than ever because score models increasingly reflect ongoing behavior, especially balance trends and payment consistency, not just a dispute outcome from three months ago.

Here is what a smart, 2026-aligned credit repair plan looks like in practice:

- Reduce revolving utilization month over month. Even small reductions, say from 35% to 33% to 31%, signal positive momentum to trended data models. Do not wait to make one big payoff. Chip away steadily.

- Set up autopay for at least the minimum balance. A missed payment is one of the most damaging events in credit scoring. Autopay eliminates that risk.

- Review your credit reports every 90 days. Errors do happen, and catching them quickly means faster resolution. You are entitled to free reports, and disputing genuine errors is always worth doing.

- Build positive account history proactively. A secured credit card or credit-builder loan adds positive payment history to your file over time. This is especially useful if your file is thin.

- For small businesses: maintain and update your business credit profile. Many business owners have never formally registered their business credit with Dun & Bradstreet, Experian Business, or Equifax Business. In 2026, fintech lenders and traditional banks alike are checking these profiles as part of underwriting.

Pro Tip: Ask your vendors whether they report payment history to commercial credit bureaus. If they do, paying your business invoices on time builds your business credit profile automatically, at no extra cost to you.

Following structured credit repair steps can help you organize these actions into a realistic timeline. And if your goal is bigger than just fixing your score, the path toward achieving financial freedom through credit repair is worth exploring as a longer-term framework.

What most credit repair advice misses in 2026

With the best practices laid out, here is a candid view of what most people and even some experts are still missing.

The credit repair industry has been obsessed with disputes for decades. Dispute this account. Challenge that inquiry. Send certified letters until something disappears. And yes, disputing genuine errors is legitimate and important. But the conversation has been so dominated by disputes that most consumers never focus on the underlying behavioral patterns that now drive the majority of score movement.

Here is the uncomfortable truth: ongoing behavior is more important than any single dispute when it comes to score improvement in 2026. If your balances are high, inconsistent, or growing, no amount of disputing will move your score meaningfully. You can clean up your report perfectly and still get denied for a mortgage because your 24-month utilization trend signals financial stress to the lender’s model.

For small business owners, this gap in understanding is even more costly. The 2026 Federal Small Business report highlights that lending access for small businesses increasingly depends on the full financial picture, not just a credit score. A business owner who has done everything right on the personal credit side but has no formal business credit profile, inconsistent revenue records, or unorganized financials will still struggle to access capital.

Smart credit repair in 2026 means treating your credit as a financial system that needs ongoing management. It means understanding how the lender you are applying to actually evaluates risk, because a community bank uses different criteria than a fintech lender. It means building habits around debt reduction, not just score chasing. And it means recognizing that both personal and business credit paths are evolving together with alternative and trended data playing bigger roles every year.

The resource on reversing credit repair pitfalls is a good starting point if you realize some of your current habits are working against you.

Next steps: Get help with credit repair for 2026

The trends covered in this article represent a real shift in how credit repair works, and staying ahead of those changes is the difference between a score that stagnates and one that grows consistently.

At Credit Rebooter, our tools and resources are designed specifically for this 2026 environment. Whether you are an individual working to qualify for a home loan or a small business owner trying to access capital, we have structured guidance that aligns with how lenders and scoring models actually evaluate credit today. Start with our credit score repair tools to understand exactly where you stand, and explore our credit building strategies to map out your path forward. The landscape has changed. The right support makes all the difference.

Frequently asked questions

What is trended data and why does it matter in 2026?

Trended data tracks your payment and balance behavior across multiple months, and models like FICO 10T and VantageScore 4.0 use this to evaluate whether your credit behavior signals long-term financial responsibility. It rewards consistency, not just a clean snapshot on the day you apply.

Is it legal for a credit repair company to charge me before doing any work?

No. The Credit Repair Organizations Act prohibits charging before services are fully performed. Any company that requires upfront payment is violating federal law.

What’s the average credit score in 2026?

The average VantageScore 4.0 was reported at 701 as of March 2026, with consumers actively reducing card balances and delinquency rates trending down.

Are quick credit-fixing hacks still effective?

Modern scoring models reward positive long-term behavior, not isolated disputes or one-time payoffs. Short-term hacks rarely produce lasting score improvements under trended data models.

Do small businesses need different credit repair strategies than individuals?

Yes. Small business credit repair also involves lender-fit analysis, business profile maintenance, and trended commercial data, factors outlined in the 2026 Federal Small Business report as increasingly central to lending access decisions.