Most Americans can access their credit reports for free every single week, yet millions never look. That gap costs people real money. A single error on your credit report can lower your score by dozens of points, which means higher interest rates, loan denials, and missed opportunities like buying a home or launching a business. The three major bureaus — Equifax, Experian, and TransUnion — maintain these records, and the data they hold shapes nearly every financial decision made about you. This guide breaks down what a credit report contains, how to read it, how to fix mistakes, and how to use what you learn to build real financial momentum.

Table of Contents

- What is a credit report and why it matters

- Key sections of a credit report explained

- How to check your credit report for free and how often

- How to find and dispute errors on your credit report

- How credit reports impact your credit score and financial decisions

- Our take: What most people miss about credit reports

- Take the next step: Reboot your credit journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Access is free | You can check your credit reports weekly from all major bureaus at no cost. |

| Errors are common | Mistakes like wrong accounts or outdated info can be fixed if you know what to look for. |

| Reports drive scores | Every detail on your credit report directly impacts your credit score and financial opportunities. |

| Monitoring matters | Regularly reviewing your report protects you from fraud and helps you manage your financial future. |

| Dispute process protects you | Federal law requires bureaus to investigate disputes, giving you the power to correct mistakes. |

What is a credit report and why it matters

A credit report is a detailed record of your credit history, compiled by a credit bureau (also called a reporting agency). It is not the same as your credit score. Think of it this way: the report is the raw data, and the score is the grade calculated from that data. Understanding the difference is one of the first steps toward taking control of your credit report and score.

According to the CFPB, credit reports include your personal information, open and closed accounts, payment history, inquiries, and public records. Lenders use this information to decide whether to approve your application and at what interest rate. Landlords check it before handing over a lease. Insurers may review it when setting premiums. Even some employers pull a version of it during background checks.

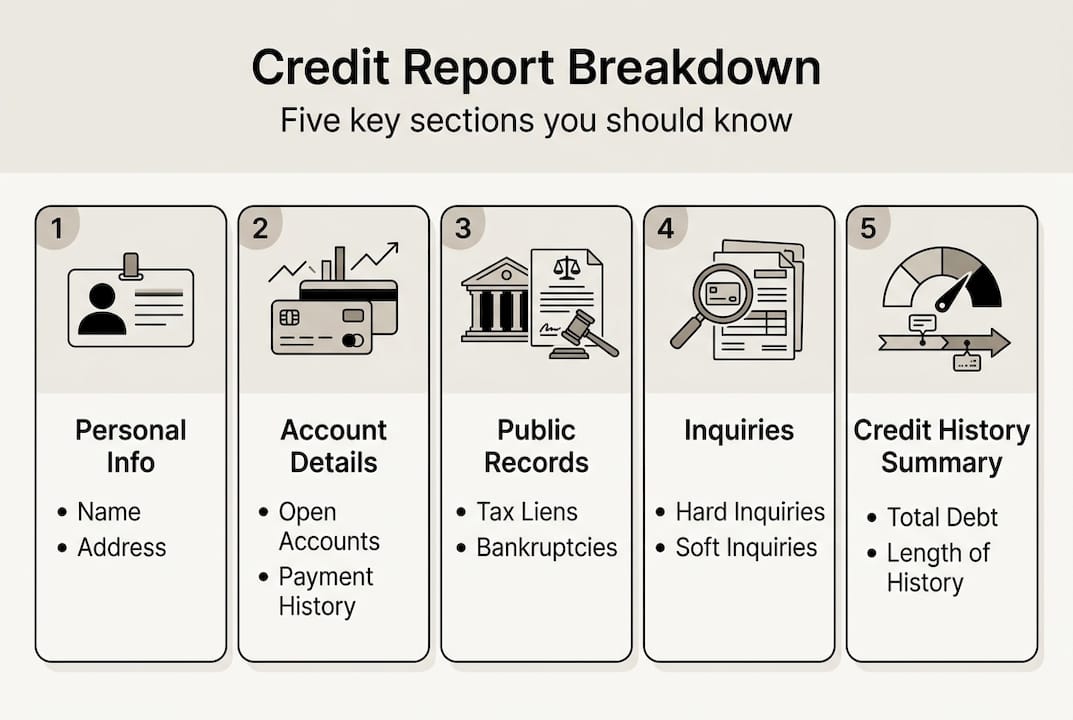

Here is a snapshot of what a standard credit report contains:

| Section | What it includes |

|---|---|

| Personal information | Name, address history, Social Security number, date of birth |

| Account history | Credit cards, mortgages, auto loans, student loans |

| Payment history | On-time payments, late payments, missed payments |

| Inquiries | Hard and soft credit checks |

| Public records | Bankruptcies, civil judgments, tax liens |

For small business owners, this matters even more. Many lenders check your personal credit first before they consider your business credit, especially for startups and businesses with limited financial history. So a strong personal report can open doors for both your life and your business.

Key things every report contains:

- Your full account history going back up to 10 years

- Who has recently checked your credit

- Whether any accounts have gone to collections

- Any public financial records tied to your name

To understand what your credit report score actually reflects, you need to understand this underlying data first. The report is where the real story lives.

Key sections of a credit report explained

With a clear sense of what a credit report includes, let’s break down each section and see what it means for your financial life.

A typical credit report has five main sections. Each one tells a different part of your financial story, and each carries different weight with lenders. The CFPB confirms that these five sections — personal information, accounts, payment history, inquiries, and public records — are the standard components across all three bureaus.

Here is how individuals and small business owners should interpret each section differently:

| Section | What an individual looks for | What a business owner looks for |

|---|---|---|

| Personal information | Confirm accuracy of name and address | Ensure no business activity is mistakenly tied to personal info |

| Accounts | Check balances and credit limits | Look at credit utilization across personal and business lines |

| Payment history | Spot any late payments | Identify patterns that affect business loan eligibility |

| Inquiries | See who has checked your credit | Limit hard pulls when seeking business financing |

| Public records | Confirm no incorrect judgments | Watch for liens that could block business funding |

Here is how to read each section step by step:

- Personal information — Confirm your name is spelled correctly, all addresses are yours, and your Social Security number is accurate. Even a small mismatch can flag your file.

- Accounts — Review each account listed. Confirm it belongs to you, the balance is correct, and the account status (open or closed) is accurate.

- Payment history — This section alone accounts for 35% of your FICO score. A single late payment listed in error can drag your score down significantly.

- Inquiries — Hard inquiries (when a lender checks your credit with your permission) can slightly lower your score and stay on your report for two years. Soft inquiries (like checking your own report) do not affect your score at all.

- Public records — Bankruptcies stay on your report for 7 to 10 years. If one appears that is not yours, that is a red flag requiring immediate action.

Common red flags include accounts you do not recognize, payments marked late when you paid on time, and balances that do not match your records. Reviewing report score meanings alongside your raw report gives you the full picture.

Pro Tip: Pull all three bureau reports at the same time for your first review. They often contain different information, and comparing them side by side helps you spot discrepancies much faster. You can also explore facts about credit scores to understand how each section influences your overall number.

How to check your credit report for free and how often

Knowing the value of each section, the next step is actually getting your hands on your credit reports, quickly and safely.

The official government-authorized site for free credit reports is AnnualCreditReport.com. This is the only federally mandated free access point, and it will never ask you to pay or enter a credit card number. As of 2026, free weekly access to all three credit bureau reports is available to every American, a benefit that became permanent following changes made during the pandemic era.

Here is how to check your report safely:

- Visit AnnualCreditReport.com directly (type it manually, do not click links in emails)

- Choose which bureau or bureaus you want to review

- Verify your identity using your Social Security number and personal history questions

- Download or print your report for review

- Look through each section carefully using the framework from the previous section

Most financial experts recommend checking your reports at least once a month. Reviewing all three bureaus quarterly at minimum gives you solid coverage. Why so often? Because fraud can appear within days of your information being stolen. Catching an unfamiliar account early, before it damages your score further, can save you months of repair work.

Pro Tip: Stagger your bureau pulls across the year if you want ongoing coverage without information overlap. Pull Equifax in January, Experian in May, and TransUnion in September for a rotating review schedule.

One critical fact that surprises many people: checking your own credit report does not lower your score. It counts as a soft inquiry, which is invisible to lenders and has zero impact on your number. So there is no reason to avoid looking. Use credit improvement tips alongside your report reviews to turn what you find into a concrete action plan.

How to find and dispute errors on your credit report

After you have checked your report, it is time to make sure what is listed is accurate — and fix it fast if something is wrong.

Errors on credit reports are more common than most people expect. Incorrect personal information, duplicate accounts, payments marked late when they were on time, and outdated balances are among the most frequent problems. Sometimes these errors happen because of a data entry mistake. Sometimes they result from identity theft. Either way, the impact is real and the fix is your legal right.

The most common errors to watch for:

- Wrong name or address — Could indicate a mixed file with someone who has a similar name.

- Accounts that are not yours — A sign of identity theft or a bureau data merge error.

- Incorrect payment status — Payments listed as late when you have proof they were on time.

- Duplicate accounts — The same debt listed twice, inflating your total owed.

- Outdated negative entries — Most negative items must be removed after seven years by law.

Here is how to dispute an error under the Fair Credit Reporting Act (FCRA):

- Gather your documentation. Bank statements, receipts, or correspondence that prove the error.

- Submit your dispute to the bureau (online, by mail, or by phone) and to the original creditor.

- Include copies, not originals, of all supporting documents.

- The bureau has 30 days to investigate and respond, as required by the FCRA.

- If the error is confirmed, the bureau must correct or remove it.

Your rights matter. Under federal law, credit bureaus must investigate your dispute within 30 days and notify you of the outcome. If the item is not corrected, you have the right to add a 100-word statement to your file explaining your position.

Pro Tip: Send dispute letters by certified mail with return receipt requested. This creates a legal paper trail that protects you if the bureau fails to respond within the required window.

For more guidance on putting your plan into action, explore repairing your credit and improving your credit with proven step-by-step approaches. You can also review the full FTC instructions for disputing errors directly.

How credit reports impact your credit score and financial decisions

Now that errors are out of the way, discover how your credit report’s information actually shapes your financial future.

Every item on your report either helps or hurts your score. And your score determines a lot: mortgage rates, credit card APRs, auto loan terms, even your ability to rent an apartment. The CFPB makes clear that paying on time and keeping balances low are the two most powerful habits for protecting your creditworthiness, and both are reflected directly in your report.

Here are the habits that move the needle most:

- Pay on time, every time. Payment history is 35% of your FICO score. Even one 30-day late payment can drop your score by 50 to 100 points.

- Keep your credit utilization below 30%. If your card limit is $10,000, keep your balance under $3,000. Lower is better.

- Avoid opening too many accounts at once. Each hard inquiry can shave a few points off your score temporarily.

- Keep older accounts open. Length of credit history matters. Closing an old card can shorten your average account age.

- Diversify your credit mix. A healthy mix of installment loans and revolving credit tends to score better than just one type.

For small business owners, this gets more important. Lenders evaluating a business line of credit or SBA loan will often look at your personal report alongside any business credit profile. A personal score below 650 can disqualify you even if your business revenue looks strong. Actively working on improving your score is not just personal finance — it is a business strategy.

The bottom line: your credit report is a live document. It updates monthly as creditors report new information. Building good habits now creates a ripple effect that shows up in your report, your score, and ultimately the rates and opportunities you can access.

Our take: What most people miss about credit reports

Stepping back from the how-to details, here is what our experience reveals about real-world credit report mastery.

Most people treat their credit report like a fire alarm — they only look at it when something is already burning. By that point, the damage is done. The truth is, your report is more like a financial dashboard. It tells you where you are, where you have been, and — if you know how to read it — where you are headed.

One thing we see constantly: people miss early signs of identity theft because they go years without checking their reports. A fraudulent account opened in your name and left unpaid for 12 months can devastate a score that took years to build.

The other thing most people underestimate is how a monthly review habit builds genuine financial confidence. When you understand what is on your credit score facts dashboard, you stop guessing whether you will qualify for a loan. You know. That shift — from anxiety to clarity — is more powerful than any single credit repair tactic. Treat your report like your monthly budget review, not a once-a-year event.

Take the next step: Reboot your credit journey

If you are ready to put these lessons to work and take control, here is where tailored guidance can help.

Understanding your credit report is only the first step. Acting on that knowledge is where real change happens. Whether you need to correct errors, build a stronger history, or adopt smarter habits, Credit Rebooter offers tools and resources designed for your specific situation.

Explore our credit score repair resources to tackle negative marks head-on. If you are starting from scratch or rebuilding after setbacks, our guidance on building credit history and credit building strategies can help you create a roadmap that works. You do not have to figure this out alone. We are here to help you move from confusion to confidence, one step at a time.

Frequently asked questions

How can I get my credit report for free in 2026?

Visit AnnualCreditReport.com to access your Equifax, Experian, and TransUnion reports at no cost. As confirmed by the CFPB, free weekly access to all three reports is available to every American.

How do I dispute an error on my credit report?

Submit your dispute in writing, online, or by phone to the credit bureau and the original creditor, along with supporting documents. Under the FCRA, bureaus must investigate within 30 days and notify you of the outcome.

Will checking my own credit report hurt my credit score?

No. Checking your own report counts as a soft inquiry, which is not visible to lenders and has no impact on score. You can review your reports as often as you like without any penalty.

What are the most common mistakes found in credit reports?

The most frequent errors include incorrect personal information, duplicate accounts, and outdated or wrong account statuses. The FTC notes that common report errors can often be corrected once you file a formal dispute with documentation.