Nearly half of small business loan applications face rejection, and 20% of denials come down to one thing: low or missing business credit. That’s not a financing problem. It’s a knowledge problem. Most small business owners pour energy into their product, their team, and their customers, but never learn how business credit actually works until a lender says no. This guide changes that. You’ll learn exactly what small business credit is, how it’s scored, how to build it from zero, how to protect it, and how to use it to grow your business and land better deals.

Table of Contents

- Understanding small business credit: The basics explained

- How to build small business credit from scratch

- Avoiding pitfalls and credit score killers

- Using small business credit: Growth, financing, and smart strategies

- Why most small business credit advice misses the real challenge

- How Credit Rebooter can help your business credit journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Business credit basics | Small business credit is your company’s financial trust factor for lenders and vendors. |

| Establishing credit | Forming a legal entity, opening tradelines, and early payments lay a strong foundation. |

| Avoiding mistakes | Check credit bureau reports quarterly and use only vendors that report to bureaus. |

| Financing success | Higher scores and more tradelines improve your odds for loans and better terms. |

Understanding small business credit: The basics explained

With that challenge in mind, let’s break down exactly what small business credit means and why it matters.

Small business credit is your company’s financial track record. It shows lenders, suppliers, and partners how reliably your business borrows and repays money. Think of it as a report card for your company’s financial behavior, completely separate from your personal credit score.

The separation matters more than most people realize. Personal credit reflects your individual borrowing history. Business credit reflects your company’s history. Lenders, vendors, and even potential business partners check your business credit to decide whether to extend terms, approve financing, or enter into contracts with you. Without it, you’re invisible or worse, you look risky.

Key components of a business credit profile:

- Business structure: Your legal entity (LLC, S-Corp, sole proprietor) signals legitimacy to creditors

- EIN (Employer Identification Number): The tax ID that separates your business identity from your personal one

- Tradelines: Credit accounts reported to business bureaus, such as vendor accounts, credit cards, and loans

- Payment history: The single biggest factor in most business credit scores

- Business credit bureaus: Dun & Bradstreet, Experian Business, and Equifax Business each maintain separate files

Three major scoring models dominate the business credit world. Dun & Bradstreet’s PAYDEX score runs from 0 to 100, where 80 or above signals good standing. The FICO SBSS (Small Business Scoring Service) runs from 0 to 300 and is used heavily by the SBA and banks. Experian’s Intelliscore also runs 0 to 100. Each model weighs factors differently, but payment history drives 80 to 100% of most business credit scores.

| Scoring Model | Range | Primary Use | Key Factor |

|---|---|---|---|

| D&B PAYDEX | 0 to 100 | Vendor/supplier decisions | Payment timing |

| FICO SBSS | 0 to 300 | SBA loans, bank loans | Multiple factors |

| Experian Intelliscore | 0 to 100 | Lender and vendor checks | Payment history |

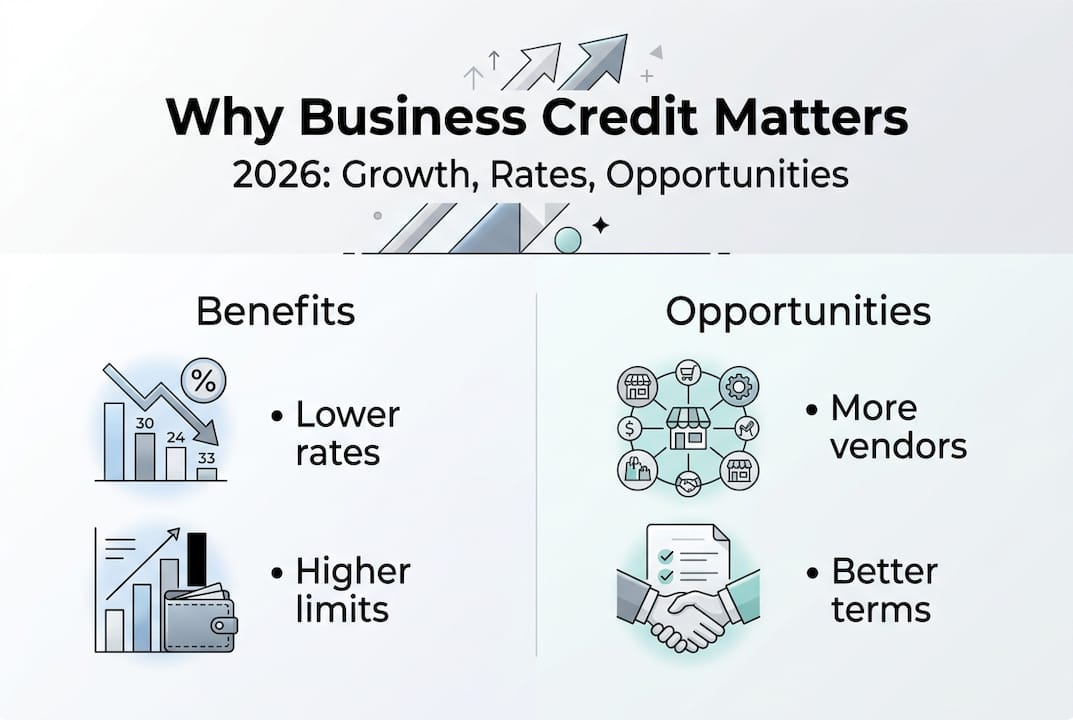

Why does strong business credit matter beyond just loan approvals? Lower interest rates, higher credit limits, net-30 or net-60 vendor terms without upfront payment, and the ability to keep your personal finances out of business decisions. You can explore more about building credit history to understand the long game. Proper registering a business as a legal entity is also step one before any credit building can begin.

How to build small business credit from scratch

Now that you know what small business credit is, let’s get specific about how you actually build it from scratch.

Establishing a legal entity, getting an EIN and DUNS number, and opening a business bank account are the foundational steps before any credit building can happen. Skip these and nothing else works.

Step-by-step process to build business credit:

- Choose your legal entity. Register as an LLC, corporation, or partnership. Sole proprietors have no legal separation, which makes credit building much harder.

- Get your EIN. Apply free through the IRS. This is your business’s tax ID and the anchor for all credit files.

- Get a DUNS number. Dun & Bradstreet issues these free. It’s required for many vendor accounts and government contracts.

- Open a dedicated business bank account. Use it exclusively for business transactions. This establishes financial legitimacy.

- Apply for net-30 vendor accounts. These vendors extend 30-day payment terms and report to business bureaus. Start with suppliers like Uline, Quill, or Grainger.

- Pay early, not just on time. PAYDEX rewards early payment with higher scores.

- Add a business credit card. Choose one that reports to business bureaus, not just personal ones.

- Monitor and maintain. Check your profiles at all three major bureaus regularly.

Net-30 vendors are the fastest entry point for new businesses. They extend credit without requiring an established score, and they report your payment behavior to bureaus. You need at least 3 to 5 reporting tradelines to generate a meaningful credit score. Fewer than that and most bureaus won’t produce a score at all.

| Tradeline Type | Reports To | Time to Score Impact |

|---|---|---|

| Net-30 vendor account | D&B, Experian | 30 to 60 days |

| Business credit card | Experian, Equifax | 30 to 60 days |

| Business loan | All three bureaus | 30 to 90 days |

| Business line of credit | All three bureaus | 30 to 90 days |

Most businesses can expect their first score within 6 to 12 months of consistent activity. The establishing business credit process rewards patience and consistency, not shortcuts.

Pro Tip: Pay invoices 5 to 10 days early whenever possible. On-time payment earns an 80 PAYDEX. Early payment pushes you to 100. That difference can mean better vendor terms and lower financing costs. Check out credit building ideas for more ways to accelerate your profile.

Avoiding pitfalls and credit score killers

Once you start building credit, it’s just as important to avoid the mistakes that can quietly sabotage your progress.

The most damaging mistake is mixing personal and business finances. When you use personal accounts for business expenses or personally guarantee every business debt, lenders can’t distinguish your business risk from your personal risk. That confusion leads to denials.

Common mistakes that damage business credit:

- Late payments: Even one late payment can drop your PAYDEX score significantly

- High credit utilization: Using more than 30% of available credit signals financial stress

- Too many credit applications at once: Multiple hard inquiries in a short window raise red flags

- Incorrect business information: Mismatched addresses, names, or phone numbers across bureaus create confusion and lower scores

- Using vendors that don’t report: Not all vendor accounts report to bureaus, so activity on those accounts builds nothing

Errors are common on business credit reports, too many credit inquiries can hurt, and not all vendors report to the major bureaus. This means you can do everything right and still have a weak profile if you’re not paying attention to where your activity is being recorded.

Important: Your business credit file is not automatically corrected when errors appear. You must actively dispute mistakes with each bureau individually. Dun & Bradstreet, Experian Business, and Equifax Business each have their own dispute processes.

To dispute errors, pull your reports from all three bureaus, identify any incorrect tradelines, payment records, or company data, and submit a formal dispute with documentation. The process can take 30 to 60 days. Learn how to approach steps for credit repair and get familiar with reviewing credit files so you know exactly what to look for.

Pro Tip: Set a quarterly calendar reminder to pull your business credit reports from all three major bureaus. Catching an error early is far easier than fixing months of compounding damage.

Using small business credit: Growth, financing, and smart strategies

After protecting your credit foundation, here’s how to actively use it to help your company grow and secure better deals.

Strong business credit is not just a defensive tool. It’s a growth lever. Bank loan and line of credit approval rates climb sharply for businesses with higher FICO scores and established credit histories. Businesses with thin or no credit profiles face rejection rates well above 50% for traditional bank loans.

| Credit Strength | Typical Loan Approval Rate | Average Interest Rate Range |

|---|---|---|

| Strong (FICO 700+) | 60 to 80% | 6 to 10% |

| Moderate (FICO 600 to 699) | 30 to 50% | 12 to 20% |

| Weak (FICO below 600) | Under 20% | 20%+ or denied |

Here’s how to put your business credit to work:

- Apply for a business line of credit. Lines of credit give you flexible access to cash for inventory, payroll gaps, or growth opportunities.

- Negotiate better vendor terms. Strong credit lets you request net-60 or net-90 terms, improving your cash flow without borrowing.

- Apply for SBA loans. The SBA uses FICO SBSS scores heavily. A score above 155 is generally required for SBA 7(a) loans.

- Use business credit cards strategically. Keep utilization below 30% and pay in full monthly to build credit while earning rewards.

- Diversify your credit types. A mix of revolving credit (cards) and installment credit (loans) signals financial maturity to lenders.

Smart business credit card usage is one of the fastest ways to build a diverse credit profile while managing day-to-day expenses. Combine that with consistent loan payments and you create a profile that lenders genuinely want to work with. For deeper strategies, explore building strong credit and repairing and building credit to cover all your bases.

Why most small business credit advice misses the real challenge

With all the facts laid out, let’s go beyond the basics and talk about what really makes or breaks business credit in practice.

Most guides give you the checklist and stop there. Get an EIN. Open a bank account. Pay on time. Done. But the reality is messier. Bureaus are slow to update. Vendors you trusted to report sometimes don’t. Errors appear from nowhere and sit on your file for months before you notice. Personal credit bleeds into business decisions even when you’ve done everything right, especially in the first two years.

We call this the hidden bureaucracy tax. It’s the time, energy, and money you lose not because you made bad financial decisions, but because you didn’t know the system well enough to catch its mistakes. The businesses that build great credit fastest are not the ones with secret vendor lists or credit hacks. They’re the ones who treat their building strong credit history like a business process: scheduled check-ins, documented disputes, and consistent follow-through.

No automation handles this for you. Your diligence is the strategy.

How Credit Rebooter can help your business credit journey

Ready to take charge of your small business credit success? Here’s how Credit Rebooter supports your journey.

Building business credit is straightforward when you know the steps, but staying on track takes consistent effort and the right tools. Credit Rebooter offers tailored resources for small business owners at every stage, whether you’re starting from zero or cleaning up a damaged profile.

From proven credit building strategies to a structured credit repair system designed for real results, Credit Rebooter gives you the guidance and support to move faster and avoid costly mistakes. You can also explore resources on building credit history to strengthen your foundation at every step. Your business deserves credit that works as hard as you do.

Frequently asked questions

How long does it take to build small business credit?

Most businesses can build an initial credit profile and score in 6 to 12 months with consistent tradeline activity and on-time payments.

Do personal and business credit affect each other?

Early on, personal credit often impacts business approval decisions, especially for startups and sole proprietors, but strong business credit can separate your profiles over time.

What are business tradelines, and why do they matter?

Tradelines are credit accounts reported to business bureaus, and having 3 to 5 tradelines reporting consistently is the minimum needed to generate a meaningful business credit score.

Can errors on my business credit report be fixed?

Yes, errors should be disputed promptly with each bureau individually, since business credit files are not automatically corrected.

Why did my loan application get denied even with some business credit?

Approval rates are highest for established credit and high FICO scores, and 20% of loan denials are tied to low credit, often caused by too few tradelines, a short history, or unresolved errors.

Recommended

- 101 Useful Building Credit Ideas | Credit Rebooter

- Building Credit To A Better Future | Credit Rebooter

- Small Business Credit Checklist For Better Financing

- Build Credit In Your Name | Credit Rebooter

- Small business insurance California 2026: 30% underinsured – Jenkins Insurance Agency Inc.

- Essential Financial Metrics Every Business Owner Needs