A 20-point difference in your credit score can cost you thousands of dollars over the life of a mortgage. That’s not a typo. Most people assume credit scores are just a number lenders glance at before approving a loan, but the reality is far more consequential. Whether you’re saving up to buy a home, finance a vehicle, or acquire a small business, your credit score shapes what you pay, what you qualify for, and how fast you can move. This guide breaks down exactly what your score means, why it matters for both personal and business goals, and what practical steps you can take today to improve it.

Table of Contents

- What is a credit score and how is it calculated?

- Why credit scores matter for individuals

- The importance of business credit scores for small business owners

- How to improve your credit score: Practical strategies

- The overlooked truth about credit scores: It’s not just the number

- Take charge of your credit future with Credit Rebooter

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Credit impacts costs | Higher credit scores save you thousands on loans and insurance over your lifetime. |

| Multiple score factors | Payment history and credit utilization are the most important factors for a strong score. |

| Strategies work fast | Reducing utilization and fixing errors can raise your score by 20–100 points quickly. |

| Business credit matters | Small business owners need strong business scores for loans and growth opportunities. |

| Credit isn’t everything | Lenders consider credit, income, and cash flow together for important decisions. |

What is a credit score and how is it calculated?

A credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness to lenders, landlords, and financial institutions. In the U.S., the two dominant scoring models are FICO and VantageScore. FICO is used in roughly 90% of lending decisions, making it the standard most worth understanding. You can brush up on the fundamentals by reviewing credit score basics before diving into strategy.

Here’s how FICO calculates your score:

| Factor | Weight | What it signals |

|---|---|---|

| Payment history | 35% | Whether you pay bills on time |

| Credit utilization | 30% | How much of your available credit you use |

| Length of credit history | 15% | How long your accounts have been open |

| New credit | 10% | Recent applications or new accounts |

| Credit mix | 10% | Variety of credit types (cards, loans, etc.) |

Each factor tells a lender something specific about your financial behavior. Payment history is the single largest factor because it answers the most basic question: will this person actually pay me back? Credit utilization matters because using too much of your available credit signals financial stress, even if you pay in full every month.

Here’s what each factor means in plain terms:

- Payment history: One missed payment can damage your score significantly. Lenders see consistent on-time payments as reliability.

- Credit utilization: Keeping balances low relative to your credit limits signals discipline. The lower, the better.

- Length of history: Older accounts demonstrate a longer track record. This is why closing old cards can actually hurt you.

- New credit: Every time you apply for credit, a hard inquiry is recorded. Too many in a short period looks risky.

- Credit mix: Having both revolving credit (like cards) and installment loans (like car payments) shows versatility.

Pro Tip: Keeping your credit utilization below 10% gives you the best shot at reaching the highest score tiers. Even if 30% is the common guideline, elite scorers stay well under that.

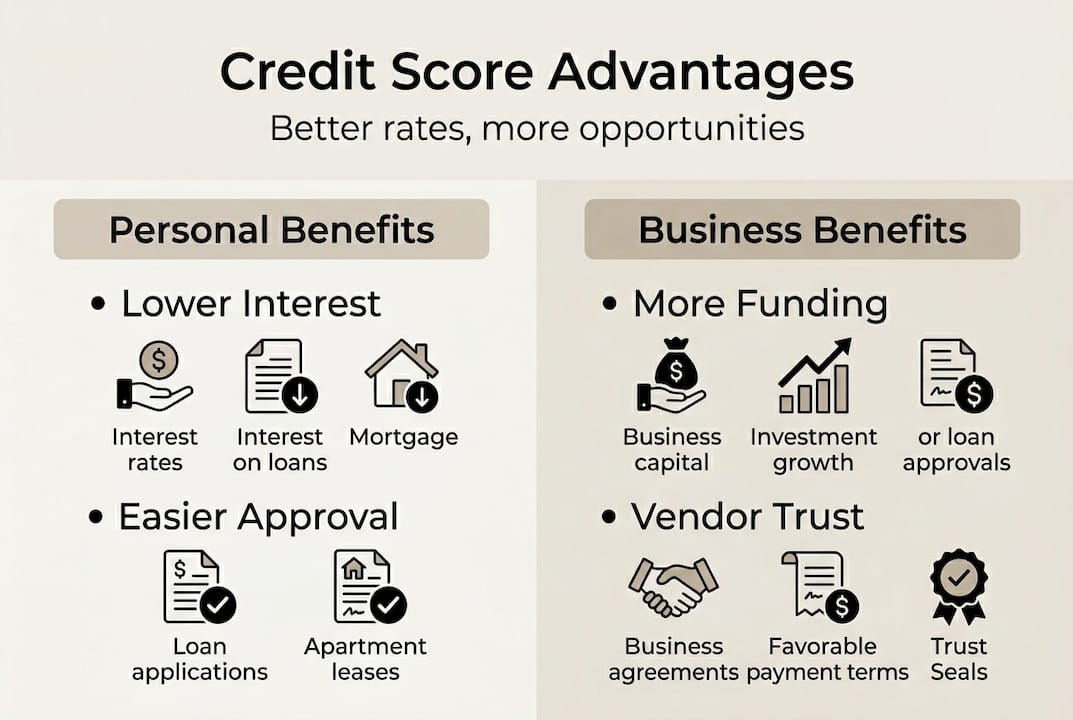

Why credit scores matter for individuals

With the basics in mind, let’s see why personal credit scores are gateways to better financial opportunities. Your score determines far more than just loan approval. It controls the interest rate attached to that approval, which changes the total cost of everything you borrow.

A FICO score of 760+ can save you between $10,000 and $46,000 over the life of a mortgage compared to borrowers in lower score tiers. Here’s how score ranges generally translate to mortgage rate differences:

| FICO Score Range | Credit Tier | Relative Rate Impact |

|---|---|---|

| 760 and above | Excellent | Best available rates |

| 700 to 759 | Good | Slightly above best |

| 650 to 699 | Fair | Noticeably higher rates |

| Below 650 | Poor | Significantly higher rates or denial |

Beyond mortgages, your score affects:

- Car loan rates: Lower scores can add hundreds of dollars per year in interest on an auto loan.

- Credit card APRs: A weak score can land you in a high-rate card, making it harder to pay down balances.

- Insurance premiums: Many insurers use credit-based scoring to set home and auto insurance rates.

- Rental housing: Landlords routinely screen applicants by credit score, and low scores can disqualify you.

- Personal loan access: Unsecured personal loans become either expensive or unavailable below certain score thresholds.

One statistic worth knowing: a single 30-day late payment can drop your score by 90 to 110 points. That’s the equivalent of falling from a good credit tier to a poor one in a single month. Building solid credit habits is the most reliable way to protect what you’ve built.

Pro Tip: Set up autopay for at least the minimum payment on every account. Even if you plan to pay more, this guarantees you never accidentally miss a due date.

The importance of business credit scores for small business owners

Individuals aren’t the only ones affected. Business owners face even greater stakes if credit scores are overlooked. Your business has its own credit profile, separate from yours, and business credit scores from agencies like D&B, Experian, Equifax, and the FICO SBSS system affect your access to loans, vendor payment terms, insurance rates, and more.

Here’s a snapshot of the main business credit scoring systems:

| Agency | Score Range | “Good” Score Threshold |

|---|---|---|

| D&B PAYDEX | 0 to 100 | 80 and above |

| Experian Intelliscore | 1 to 100 | 76 and above |

| Equifax Business | 101 to 992 | 500 and above |

| FICO SBSS | 0 to 300 | 160+ for SBA loans |

Keeping personal and business credit separate matters more than most small business owners realize. When your business has its own credit profile, you protect your personal assets from business liabilities and unlock financing that doesn’t depend entirely on your personal score. You can learn more about establishing business credit as an independent financial identity.

Here are the key steps to build business credit alongside personal credit:

- Incorporate your business (LLC or corporation) and get an EIN from the IRS.

- Open a dedicated business checking account and business credit card.

- Register with D&B to get a DUNS number, which creates your business credit profile.

- Pay all business bills early or on time, since payment history matters here too.

- Work with vendors who report payment history to business credit bureaus.

SBA loans often review both your personal FICO score and your FICO SBSS score. If one is weak, it can block access to programs with the lowest rates and best terms.

Pro Tip: Open trade lines with vendors who report to business credit bureaus. Suppliers like Quill, Grainger, or Uline often offer net-30 accounts that build your business profile faster than most other methods.

How to improve your credit score: Practical strategies

Understanding personal and business credit scores is half the battle. Here’s how to make tangible progress, fast.

The most actionable sequence for improving your score looks like this:

- Pay every bill on time: Payment history carries the most weight. Even one missed payment causes disproportionate damage.

- Lower your credit utilization: Pay down balances to get below 30%, and ideally below 10%, of your total available credit.

- Dispute errors on your credit report: Over 20% of reports contain errors, and disputing them can yield 25 to 100 point gains.

- Avoid new credit applications: Each hard inquiry costs a few points. Space out applications at least 6 to 12 months apart.

- Diversify your credit mix: If you only have credit cards, consider a small personal loan or credit-builder loan to add variety.

- Become an authorized user: Being added to a family member’s old, well-managed card can boost your score quickly.

“You can gain 20 to 50 points quickly by lowering utilization, and 25 to 100 points by disputing errors on your credit report.”

Some situations require a tailored approach. If you have a thin file (fewer than 4 accounts), traditional scoring may not capture your full picture. Newer models like FICO 10T use trended data, meaning your direction of travel matters, not just your current balance. If you’ve had medical debt removed from collections or are working through authorized user strategies, you may see faster gains than average.

Common pitfalls to avoid:

- Closing old accounts to “clean up” your profile (this shortens your history and raises utilization)

- Ignoring business credit while building personal credit

- Pulling your credit from only one bureau and assuming all three are the same

- Applying for several new accounts in a short period to build credit faster

For more credit improvement ideas based on your specific situation, it helps to have a structured plan rather than random actions. If you’re already making progress and want to accelerate it, you can find step-by-step guidance on improving your score built around your current profile.

The overlooked truth about credit scores: It’s not just the number

Here’s something most credit guides won’t tell you: a high credit score is necessary but not sufficient. Lenders, landlords, and SBA underwriters routinely look beyond your three-digit score. They examine your debt-to-income (DTI) ratio, your cash flow history, your income stability, and in the case of business acquisitions, your business’s earnings record.

Credit alone is often insufficient. Lenders take a holistic view, meaning two applicants with the same credit score can get very different outcomes based on income and DTI. We’ve seen clients with 740+ scores get denied because their DTI was too high, and clients with 680 scores get approved because their income was strong and their debt load was minimal.

The real lesson: don’t chase the number alone. Build the profile. That means reducing total debt, maintaining stable income, and keeping your financial behavior consistent over time. A one-time score boost from a dispute is valuable, but a score that has been above 720 for three years tells a much more compelling story to any underwriter. Credit improvement is a long-term posture, not a short-term fix.

Take charge of your credit future with Credit Rebooter

Now that you have the roadmap, here’s how to put what you’ve learned into immediate practice.

Knowing the strategies is one thing. Applying them in the right sequence for your specific profile is where most people get stuck. At Credit Rebooter, we’ve helped individuals and small business owners develop business and personal credit strategies tailored to their real goals, whether that’s buying a home, qualifying for an SBA loan, or simply lowering the interest rate on existing debt.

One financial misstep doesn’t define your future. With the right support and a clear plan, real progress happens faster than most people expect. Explore our credit score repair programs for a structured path forward, or start with the basics and build your credit history from the ground up. Your next financial milestone is closer than you think.

Frequently asked questions

What is considered a good credit score for buying a house?

A FICO score of 740 or higher is optimal for mortgage rates, but many lenders approve mortgages starting at 680 when other financial factors like income and DTI are strong.

How do business credit scores differ from personal credit scores?

Business credit scores track your company’s financial reliability separately from your personal score, and they use different scales. D&B PAYDEX and FICO SBSS are two of the most common business scoring systems used by lenders and suppliers.

Can I improve my credit score quickly?

Yes. Reducing your credit utilization and disputing report errors can produce 20 to 50 point gains within weeks, while consistent on-time payments create lasting improvement over months.

What other factors do lenders consider besides credit scores?

Lenders review your income, DTI ratio, and cash flow history alongside your score. According to a holistic lending view, two applicants with identical scores can receive very different loan decisions based on these additional factors.